What You Should Earn

Page 58

Page 61

If you've noticed an error in this article please click here to report it so we can fix it.

The. Importance of having Some System of Cost Recording is Stressed in this Article, which also Deals with the Minimum—daily—charge Method of Fixing Rates THE acquisition of many long-distance operators running under free enterprise has undoubtedly increased the proportion of hauliers who keep no tigures of operating costs and who have no idea of what these comprise It is still a matter of astonishment to me to find that so many have little knowledge of what to me has always seemed to be an important subject.

There appears to be no real reason for this widespread ignorance of what I would term the facts of life so far as the haulier is concerned. Some operators have never bothered to keep records and probably never will. One of the greatest difficulties in persuading them to do so is the fact that it is widely known that many hauliers make a mccess of their businesses without going to any such trouble. However. I think it is reasonable to say that where this is the case, success has not been achieved because records were lot kept but despite that neglect.

Most hauliers' charges are not founded upon any rational system of costing. They are either what can be obtained or the work in the face of competition, or are rates which have been recommended by an association. The Road Haulage Association is to be congratulated upon the manner in which it has dealt with the question of recommended rates, and that so many of its members have adhered to them so far as practicable.

Secret of Success I think that the real secret of success in those cases where a man has built up a profitable business without keeping records lies in shrewd innate bushsess sense and ability to select profitable traffics. Now and again I do find operators who keep records of their operating costs and overheads, hut methods vary so much that comparisons are almost impossible. I do not suggest that there is any lack of usefulness in any of the methods I have inspected. I always refrain from criticizing any method merely because it is unorthodox or unlike what I recommend. All I look for is the provision for entering every item of expense.

With this in mind, there is no great difficulty in making a check. So far as operating costs are concerned, there are 10 principal headings: licence, wages, garage rent, insurance, interest, fuel, lubricants, tyres, maintenance and depreciation. So long as a reasonable figure is debited against each of these items, 1 am satisfied that the haulier's idea of his expenses is fairly accurate.

Anything which can-not be included under these headings comes within establishment charges, and so far as these are concerned I follow the same principle when looking over an operator's records. I have a comprehensive list of items of overheads and I check them, seeing that the figures debited are reasonable.

Although a system of costing may not be as useful as it might be, this is as nothing compared with the fact that the operator is getting some idea of what his costs are. If a man keeps such recordsand checks his expenditure against revenue frequently, he is unlikely to pursue a policy of ratecutting—a matter against which, we still have to guard to-day and may have to beware of even more in the immediate future.

Haphazard Method One method of dealing with the subject of costs with which I have not dealt for a long time concerns the fixation of a figure for minimum earnings per day. It is a haphazard .method, but as it exists I am bound to mention it.. I must admit that I am acquainted with several big operators who use this method and make a success of it. However, it is not a procedure to be recommended to newcomers.

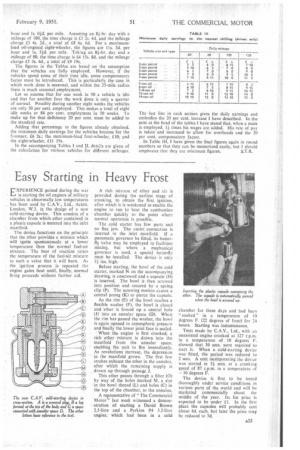

The following figures and the -accompanying tables may serve as a guide to those to whom the method appeals. The bases of the calculations are the time and mileage figures from "The Commercial Motor" Tables of Operating Costs modified to provide for the increases in items of expense that have been imposed since the Tables were published.

Taking a 30-m.p.h. 5-tonner which covers 60 miles in an 8i-hour day, the method is thus: time charge from the Tables 6s. per hr., plus 2d. for the recent wage increase and Id. for the higher insurance premiums. Another Id. is added for 20 per cent, profit and that gives a total of 6s. 4d., which is quoted in the accompanying table. Mileage charge, 9d. plus 0.4d. for recent increases in fuel and oil prices, and 0.1d. for profit giving 91d. For an 81-hr. day and 60 miles that is equivalent to £2 13s. 10d. for time and £2 7s. 6d. for mileage, a total of £5 Is. 10d.

Figures for a maximum-load four-wheeler are 7s. 4d. an

hour and Is. Old. per mile. Assuming an 81-hr. day with a mileage of 100, the time charge is £3 2s. 4d. and the mileage charge £5 4s. 2d.. a total of £8 6s. 6d. For a maximumload oil-engined eight-wheeler, the figures are I Is. 3d. per hour and Is. 31d. per mile. Taking an 84-hr. day and a mileage of 80, the time charge is £4 15s. 8d. and the mileage charge £5 3s. 4d., a total of£9 19s.

The figures in the Tables are based on the assumption that the vehicles are fully employed. • However, if the vehicles spend some of their time idle, some compensatory factor must be introduced. This is particularly the case in which work done is seasonal, and within the 25-mile radius there is much seasonal employment, Let us assume that for one week in 50 a vehicle is idle and that for another four the work done is only a quarter of normal. Possibly during another eight weeks the vehicles are only 50 per cent. employed. This makes a total of eight idle weeks or 84 per cent, employment in 50 weeks. To make up for that deficiency 20 per cent, must be added to the standard rate.

Adding that percentage to the figures already obtained, the minimum daily earnings for the vehicles become for the 5-tanner, £6 2s.; the maximum-load four-wheeler, £10; and the eight-wheeler, £11 19s.

In the accompanying Tables I and U. details are given of the calculation for various vehicles for different mileages. The -last line in each section gives the daily earnings and embodies the 20 per cent. increase I have described. In the note at the head of the tables 1 have stated that, when a mate is employed, 14 times his wages are added. His rate of pay is taken and increased to allow for overheads and the 20 per cent. compensatory factor.

In Table III, I have given the final figures again in round numbers so that they can be memorized easily, but I should emphasize that they are minimum figures. S.T.R.