1

1 2

2 3

3 4

4 5

5 6

6 7

7 8

8 9

9 10

10 11

11 12

12 13

13 14

14 15

15 16

16 17

17 18

18 19

19 20

20 21

21 22

22 23

23 24

24 25

25 26

26 27

27 28

28 29

29 30

30 31

31 32

32 33

33 34

34 35

35 36

36 37

37 38

38 39

39 40

40 41

41 42

42 43

43 44

44 45

45 46

46 47

47 48

48 49

49 50

50 51

51 52

52 53

53 54

54 55

55 56

56 57

57 58

58 59

59 60

60 61

61 62

62 63

63 64

64 65

65 66

66 67

67 68

68 69

69 70

70 71

71 72

72 73

73 74

74 75

75 76

76 77

77 78

78 79

79 80

80 81

81 82

82 83

83 84

84 85

85 86

86 87

87 88

88 89

89 90

90 91

91 92

92 93

93 94

94 95

95 96

96 97

97 98

98 99

99 100

100 101

101 102

102 103

103 104

104 105

105 106

106 107

107 108

108 109

109 110

110 111

111 112

112 113

113 114

114 115

115 116

116 117

117 118

118 119

119 120

120 121

121 122

122 123

123 124

124 125

125 126

126 127

127 128

128 129

129 130

130 131

131 132

132 133

133 134

134 135

135 136

136 137

137 138

138 139

139 140

140 141

141 142

142 143

143 144

144 145

145 146

146 147

147 148

148 149

149 150

150 151

151 152

152 The pros and cons of factoring

Page 95

Page 96

If you've noticed an error in this article please click here to report it so we can fix it.

by John Darker AMBIM

MOST of the joint stock banks now have factoring subsidiaries. The word "factor" means many things — from an agent buying on commission to a mathematical, biological or safety unit. In the business context, the first definition broadly covers the function of the companies who on both sides of the Atlantic — are experiencing astonishing growth.

In essence, the factor takes over from his client the maintenance of his sales ledger. The factor assumes responsibility for the collection of outsta nding debts and he provides an 80 per cent advance on the face value of invoices raised by the client. Regular cash statements can be furnished by the factor.

Under-capitalized Most road haulage businesses are under-capitalized. A few firms associated with large groupings may be able to look to a rich parent organization for funds to meet temporary cash-flow or investment difficulties but the vast majority of road transport contractors live on the proverbial shoe-string. When trade is tending to decline and credit is uncomfortably tight the name of the business game is cash flow. As numerous firms with a national reputation publicly proclaim that they face a crisis of cash-flow, there is small doubt that road hauliers, in general, are finding life difficult.

Though most firms with well established connections can look to their banks for overdraft facilities there is a strict limit to the amount of an overdraft which a bank manager will provide. He will want a copperbottomed guarantee that the overdraft is secured against some tangible assets. In times of credit stringency there is the chance that overdraft facilities may be withdrawn or severely contracted. If further working capital cannot be injected into a business it may founder.

It is in this context that many small and medium-sized companies are investigating the possibilities of factoring. With inflation running at 20 per cent — some say 25 per cent — road haulage firms face a constant period of adjustment of the services they provide and the rates they must charge to survive. A few months delay in recovering from customers' extra costs carried by the business heightens the problem of long-term viability. H ow tempting, therefore, to secure a fresh source of ready money immediately work has been done for the ongoing needs of the business.

If a haulier could be certain that his customers would pay up within a few days for the transport services provided, a great burden of worry would be lifted from his shoulders. The "normal" settlement terms which used to average around six weeks are now blatantly stretched by those who can get away with doing so. In his turn, the road haulier is compelled to stretch the credit offered by his suppliers not an easy matter, certainly with fuel suppliers. Yet the small road haulier is in a poor position to finance his customer's business. To the extent that he is forced to do so in a difficult financial climate he will make his own position more difficult. He will not have the resources to take advantage of purchasing discounts for prompt payment. The money owed to him for services provided cannot be used to expand arid improve his business.

One of the companies providing a factoring service is BankAmericaWilliamsCi!vnn Factors Ltd, whose managing director, Mr Ken Holland, sees considerable potential in road haulage.

The customers

Mr Holland's firm is mainly interested in road hauliers with a turnover of at least .£100,000 a .year, though firms with a smaller turnover. would not be automatically ruled out. It would also be a plus-point if the haulier concerned has a small number of principal cusromers, since the cash collection problem for a haulage concern with a wide spread of small customers would tend to be prohibitively expensive.

Considering that there are some 140 road hauliers with over 200 vehicle fleets and that the turnover of many more companies would be in excess of £100,000 a year I think it probable that Mr Holland correctly identifies an industry where factoring can be expected to make an impact. He explained that Bank AmericaWilliamsGlynn Factors Ltd provides a professionally managed complete sales ledger service incorporating preparation of the ledgers, statement of account and a programmed procedure for the collection of outstandings and credit control. The service includes advice on suitable credit limits on customers — and new customers. Once these "credit lines" have been established there is no recourse to the haulier and the factoring company accepts total responsibility for any bad debts.

The cost

How much does the service cost? For simplicity it may be divided into two parts, first interest on moneys made available, and secondly the service charge.

The interest charged on advances is likely to be similar to normal bank overdraft rates, while the service charge will vary between I and 21/2 per cent, dependent upon the work and the risks involved.

Does it make sense in present circumstances for a haulier already heavily committed to the banks and finance houses to consider factoring — at least for the normal year's agreement traditional with factoring instituitions'?

The answer to that depends on circumstances. The additional cash flow that factoring makes available is not meant to sustain pedestrian companies until times improve. It is for the well managed company that is bent on expansion and has the drive a`nd entrepreneurial skill to achieve it in a time of perplexing business difficulty.

For example, it would make sense to use additional working finance to improve vehicle utilization — if possible by double or treble shifting, Though it is well known that intensity of use makes the best possible use of assets in the form of vehicles and premises, it is surprising to find many road hauliers and even more ownaccount operators --using their vehicles for a mere five days and perhaps for single shifts on those days.

The added traffic management and administrative burden of doubleshifting needs no emphasis but is it better for management time to be spent on this expansion of the business or to spend much effort in stimulating cash flow in more conventional ways? Road hauliers often recognize the need for staff training and in the next breath they point to the virtual impossibility of releasing staff for courses. Could it not be sensible to use extra money generated through factoring to hire temporary staff while long-service employees are trained to do a better, more responsible, job?

Expanding fleets

It is probable, unhappily, that a number of road haulage companies may go to the wall as their customers cease to trade or reduce their output of goods. There will be opportunities for the confident, optimistic road hauliers to acquire smaller firms or their vehicles, if the cash resources to do so are available. History suggests that it is often the bold man with the courage to exploit prevailing circumstances who comes to the fore. In the present context, while the instinct of the majority may be to contract operations with falling market demand, a small minority of hauliers may have the guts to expand.

A number of hauliers I know have already had approaches from factoring companies. Despite the fact that many current publications and institutions agree that in the right circumstances factoring is justified, the traditional suspicion of something new discourages innovation.

It may be argued that in present circumstances fleet expansion or double-shifting is unjustified. Many hauliers would feel that their level of rates could not support the extra interest burden that factoring entails. If the credit control function is hived off to the factor what will be done with the staff now employed on this work?

It is likely that the managing directors of most small haulage firms today spend much of their time dealing with one or other of the many aspects of cash flow. The more efficient company may already be geared to the prompt submission of invoices and may know the responsible person on eal customer's staff to telephone to pre lor payment for haulage services. contrast, there are many "traffi minded" firms who accept th customers will be slow payers, toda and that undue pressure for a fastc than-usual settlement will encoura, the customer to use a competit, haulier.

Settlement cheques

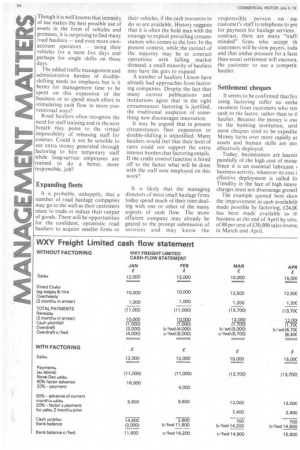

It seems to be confirmed that firr using factoring suffer no emba rassment from customers who rerr cash to the factor, rather than to ti haulier. Because the money is ow( to the banking institution, settl ment cheques tend to be expedite Money turns over more rapidly ar assets and human skills are mo effectively deployed.

Today, businessmen are learnir painfully of the high cost of mone Since it is an essential lubricant ( business activity, whatever its cost i effective deployment is called fo Timidity in the face of high intere charges must not discourage growtt The example quoted here show the improvement in cash availabilii made possible by factoring, £24,00 has been made available to tl. business at the end of April by vim. of 80 per cent of £30,000 sales revenu in March and April.