1

1 2

2 3

3 4

4 5

5 6

6 7

7 8

8 9

9 10

10 11

11 12

12 13

13 14

14 15

15 16

16 17

17 18

18 19

19 20

20 21

21 22

22 23

23 24

24 25

25 26

26 27

27 28

28 29

29 30

30 31

31 32

32 33

33 34

34 35

35 36

36 37

37 38

38 39

39 40

40 41

41 42

42 43

43 44

44 45

45 46

46 47

47 48

48 49

49 50

50 51

51 52

52 53

53 54

54 55

55 56

56 57

57 58

58 59

59 60

60 61

61 62

62 63

63 64

64 65

65 66

66 67

67 68

68 69

69 70

70 71

71 72

72 73

73 74

74 75

75 76

76 77

77 78

78 79

79 80

80 81

81 82

82 83

83 84

84 85

85 86

86 87

87 88

88 89

89 90

90 91

91 92

92 93

93 94

94 95

95 96

96 97

97 98

98 99

99 100

100 101

101 102

102 103

103 104

104 105

105 106

106 107

107 108

108 109

109 110

110 111

111 112

112 113

113 114

114 115

115 116

116 117

117 118

118 119

119 120

120 121

121 122

122 123

123 124

124 125

125 126

126 127

127 128

128 129

129 130

130 131

131 132

132 133

133 134

134 135

135 136

136 137

137 138

138 139

139 140

140 141

141 142

142 143

143 144

144 145

145 146

146 147

147 148

148 149

149 150

150 151

151 152

152 153

153 154

154 155

155 156

156 157

157 158

158 159

159 160

160 161

161 162

162 163

163 164

164 165

165 166

166 167

167 168

168 169

169 170

170 171

171 172

172 173

173 174

174 175

175 176

176 177

177 178

178 179

179 180

180 181

181 182

182 183

183 184

184 185

185 186

186 187

187 188

188 189

189 190

190 191

191 192

192 193

193 194

194 195

195 196

196 197

197 198

198 199

199 200

200 201

201 202

202 203

203 204

204 205

205 206

206 207

207 208

208 209

209 210

210 211

211 212

212 213

213 214

214 215

215 216

216 217

217 218

218 219

219 220

220 Buying a new vehicle •

Page 137

Page 138

Page 140

If you've noticed an error in this article please click here to report it so we can fix it.

should be a calculated choice

The temptation to own a brand new vehicle can be almost irresistible, but ignore the appearance and count the cost. A few minutes with the CM Tables of Operating Costs and the published performance figures might help to put the purchase in perspective.

Johnny Johnson

CONFRONTED at the Commercial Motor Show with all those shiny new vehicles, a prospective buyer could be forgiven for feeling somewhat overwhelmed and perhaps spoilt for choice. But choice, despite the visual appeal that the manufacturer has lavished on his display, should not rely on the appearance of a vehicle. The most important considerations are finance and operating cost in relation to the earning capacity of the operator' S business.

Before looking for a new vehicle, either as a first purchase or to replace an existing unit, the prudent operator will already have weighed up the relative advantages and disadvantages of acquiring a good second-hand machine as an alternative. He will have considered that certain cost factors remain the same whether the vehicle is a few years old or bought new. There is no reduction for age for road fund licences, driver's wages, insurance premiums and so on.

True, reduced expenditure can be shown, in the case of a second-hand purchase, in such items as interest on capital and depreciation but these will undoubtedly be cancelled out by increased expenditure on maintenance, higher fuel consumption and reduced Therefore, it has been assumed that after all these factors have been taken into account, the purchase of a brand new vehicle is the objective of the operator gazing enraptured at that tempting new creation labelled, "This year's model".

Getting the money

That being the case, it might be as well for him to examine just what it is going to cost him to buy it and afterwards run it. First, finding the cash. Disregarding the fortunate individual who has the necessary money ready to invest, though even he would be well advised to think of investing it elsewhere, at perhaps a steady, reliable 10 per cent or more, the practical choice lies probably between a loan from either a bank or a finance house, or hire purchase.

In omitting the possibility of raising the cash through a bank overdraft I am simply showing an awareness that in these troubled financial times a bank manager can too easily call in an overdraft, leaving the borrower adrift in a monetary sea.

Though a straight bank loan has the disadvantage of being for a comparatively short term — two or three years on average — it is attractive because the interest charge is often at a true rate of interest. That is, interest is charged currently on the capital sum outstanding. Thus if £10,000 is borrowed at 15 per cent then the first year's interest is charged on the whole sum. But supposing £3,000 is paid off the capital, then the interest charged on the second year is on the reduced capital of £7,000, and so on. There might be some difficulty in persuading a bank manager to make the loan, however, and he will inevitably expect some collateral.

In contrast, a loan from a finance house is usually an unsecured loan but the rate of interest is charged on the full capital sum over the whole of the period for which the loan is obtained. This means that the true rate of interest is equivalent to almost double the rate quoted. The current rate of interest quoted for both a loan from a finance house and a hire purchase agreement is in the order of 16.5 per cent so that the true rate is nearer 32 per cent.

Both the finance house loan and the hire purchase agreement are subject to the Hire Purchase Control Order and this means that the borrower has to find one-third of the purchase price as a deposit and the remainder is payable over 24 months.

The difference is, however, that in the case of the finance house loan the ownership of the vehicle is vested in the borrower from the commencement of the loan.

The real cost

Bearing all this in mind, the prospective vehicle buyer, should be able to calculate the real cost of the vehicle when both capital and interest are paid. From this he should be able to obtain a proper depreciation figure and the interest paid will provide the "interest on capital" factor.

These factors are two of the 10 allocations outlined in the standing and running costs detailed in Commercial Motor Tables of Operating Cosa of which the 1974 edition is now available.

The tables provide average operating costs for a range of vehicle types — not particular manufacturers' models. By comparing the average costs for particular vehicles in which the operator is interested and substituting actual figures for those shown in the tables one can get a more accurate idea of what the proposed purchase is likely to cost to operate.

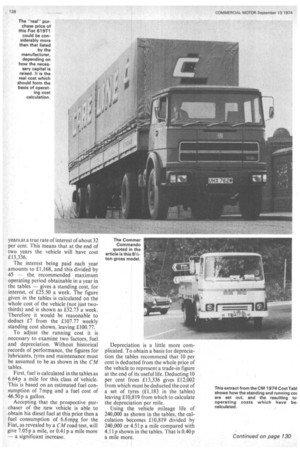

For example, take the Fiat 619T1 recently introduced (and just tested by CM). It is priced by the manufacturer at about £9,500. This price is for the 32-ton tractive unit only and it is assumed that the prospective purchaser will require a trailer to go with it. In general terms then, the complete vehicle would cost in the region of £11,000 with a flat trailer.

A loan from a finance house would involve the buyer in finding £3,670, leaving £7,330 to be paid back over two years at a true rate of interest of about 32 per cent. This means that at the end of two years the vehicle will have cost £13,336.

The interest being paid each year amounts to £1,168, and this divided by 45 — the, recommended maximum operating period obtainable in a year in the tables — gives a standing cost, for interest, of £25.50 a week. The figure given in the tables is calculated on the whole cost of the vehicle (not jtist twothirds) and is shown as E32.73 a week. Therefore it would be reasonable to deduct £7 from the £107.77 weekly standing cost shown, leaving £100.77.

To adjust the running cost it is necessary to examine two factors, fuel and depreciation. Without historical records of performance, the figures for lubricants, tyres and maintenance must be assumed to be as shown in the CM tables.

First, fuel is calculated in the tables as 6.64p a mile for this class of vehicle. This is based on an estimated fuel consumption of 7 mpg and a fuel cost of 46.50 p a gallon.

Accepting that the prospective purchaser of the new vehicle is able to obtain his diesel fuel at this price then a fuel consumption of 6.6 mpg for the Fiat, as revealed by a CM road test, will give 7.05p a mile, or 0.41 p a mile more — a significant increase. Depreciation is a little more complicated. To obtain a basis for depreciation the tables recommend that 10 per cent is deducted from the whole price of the vehicle to represent a trade-in figure at the end of its useful life. Deducting 10 per cent from £13,336 gives £12,002 from which must be deducted the cost of a set of tyres (£1,183 in the tables) leaving £10,819 from which to calculate the depreciation per mile.

Using the vehicle mileage life of 240,000 as shown in the tables, the calculation becomes £10,819 divided by 240,000 or 4.51 p a mile compared with 4.11 p shown in the tables. That is 0.40 p a mile more. The total running cost per mile of 17.75 p shown in the tables should then be increased by 0.41 p for additional fuel cost and 0.40 p for extra depreciation — giving 18.56p a mile total running cost.

How much per mile?

The total operating cost per mile then depends on the weekly mileage that the vehicle is calculated to run. Assuming an expected mileage .of 1,000 a week then the recalculated standing cost of £100.77 a week must be divided by the weekly mileage (1,000) to give 10.07p to which must be added the recalculated running cost of 18.56p a mile to give a total operating cost of 28.63 p a mile.

Translating this into an annual operating cost (28.63p multiplied by 45,000) this means that the vehicle will cost in the region of £12,883 a year to run, nearly as much as its real purchase price.

The same principle can be applied to any of the models which catch an operator's eye at the Show.

In the smaller vehicle ranges the Commer Commando at 8.5 tons gross and the Ford D0707 at 7.6 tons gross might prove interesting exercises in comparative costing. In these cases, the manufacturers' performance figures could be used, though CM road tests have shown respective fuel consumption as 15mpg and 17 mpg. Inevitably, interest will be shown in the new Leyland 165 to 250 range of vans at 1.85 tons to 2.50 tons unladen (chassis/ cab) weights.

We have just tested the low-compression petrol-engined 240 version of the new Leyland, which returned 22 mpg fuel consumption — exactly the figure given for this class of vehicle in the 1974 Cost Tables. At 46.50p per gallon, this represents a fuel cost of 2.16 pence per mile.

However, the list price of this model is £1,445 which, deducting the cost of tyres, and 10 per cent for residual value — as stated in the tables — gives a figure of £1,215 on which to base the depreciation calculation; this is £161 less than the "class average" in the tables, so will be reflected in a depreciation cost about 0.2p per mile lower than quoted in the Tables. This assumes a total useful vehicle life of 75,000 miles.

In the standing costs, the weekly interest charge for this Leyland will be £3.81 — assuming a 45-week working life per year.

Naturally, to indulge in the calculations quoted while in the noisy frantic atmosphere of the Show would probably be too much to ask. However, the prudent buyer would be well advised to take all the necessary information away with him and spend a few minutes with a pencil and paper before committing himself to buy.