Problems

Page 74

Page 75

If you've noticed an error in this article please click here to report it so we can fix it.

• of the

HAULIER and CARRIER IT may be as well to remind readers that I am dealing with the problem of finding money to pay lure-purchase instalments involved in the acquisition of a new vehicle. I have, I hope, made it clear that the amounts necessary must come out of profits. They camtbt be debited against either the operating expense of the vehicle or that of carrying on the business.

The difficulty that only too often arises is that the newcomer, who is the one usually concerned in a matter of this kind, does not make sufficient profit in the beginning, if ever, to be able to pay these instalments. I have been suggesting that it is possible, with care in the allocation of his expenditure, to pay hirepurchase instalments out of moneys properly to be allocated for subsequent and, it should be borne in mind, inevitable expense in operation.

Instalments of £3 2s. 9d. a Week.

In order to make the matter clear I have taken a concrete example relating to the purchase of a 2-tonner involving instalments equivalent to £3 2s. 9d. per week.

In the previous article, I dealt with the case of a man in an unusually favourable position. He had work to keep his vehicle einployed over a mileage of 300 per week at a fair and reasonable rate of !remuneration which was taken to be 10d. per mile run, bringing in a revenue of 112 10s. per week. I showed that his actual expenditure would be 37s. (3d. for petrol (assuming 12 m.p.g. at is. (3d. per gallon), garage rent, 10s., and wages (to himself, of course), 13 per week. Subsequent expenditure would be incurred as follows :-Oil (300 miles at 0.05d, per mile), is. 3d. ; tyres (at 0.40d.), 10s.; maintenance (at 0.44.), 11s.; depredation (at 0.54.), 13s. 6d.; taxation, 10s. (id. per week ; insurance, Ss. per week : total £2 14s. 3d. This sum, as I pointed out, must be set aside each week so that the money shall be available when needed for the purchase of supplies and the payment of tax and insurance premiums.

In this case, there would still be 14 Ss. 3d. left and, after paying £3 2s. 9d. hire-purchase instalments, a balance of 11 5s. 6d. for balance of gross profit.

Only 60 Miles a Week.

Not every 'beginner, unfortunately, is able to commence with work bringing in payment for 300 miles per week. Thb other day, for example, I had a letter from a correspondent who was going to begin, with a similar size of vehicle, and his immediate prospects comprised only one job, involving a mileage of 60 per week. In his case, the revenue would be £2 10s., the expenditure being 7s. 6d. for petrol ; 10s. garage, leaving only 11 12s. 6d. towards his own wages. Clearly, this beginner would soon be in a sad state, unless he was fortunate enough .tquickly to obtain some more work.

Now take an intermediate case, where the mileage is 380 per week. In these circumstances, assuming a revenue of 10d. per mile, the total income will be 1.7 10s. per week, expenditure on petrol will amount to 11 2s. Gd. and the addition of 10s. for garage rent brings the expenditure up to £1 12s. 6d. Clearly, there is not sufficient margin left to pay a full wage of £3 and to make provision for the hire-purchase instalment of 13 2s. Od.

Under those conditions, the haulier must inevitably forgo part of his wages. Let us assume that he allows himself 12 10s., bringing his total " drawings " to £4 2s. 6d., leaving £3 7s. 6d. Out of that, fa 2s. 9d. is put towards the monthly hire-purchase instalment, leaving 4s. 94. towards the reserve fund to provide for those items of operating cost enumerated above.

For a mileage of 180 per week, they will be as follow :-Oil, 9d.; tyres, 6s.; maintenance, Gs. 8d. ; depreciation, 8s. 2d.; tax and insurance, 18s. 6d.; total, £2 Os. 1d. There will be a shortage of £1 15s. 4d. on that reserve fund for the week and for as many weeks as the mileage remains at the figure of 180.

Now it is necessary to consider, first of all, what should be done to ensure that the reserve fund suffers as little as may be on account of this weekly deficiency.

The essential thing is to put the contribution away where it cannot easily be disturbed. Presuming that the haulier has some sort of banking account, I suggest that this 4s. 9d. be placed in the Post Office Savings Bank and the fund be allowed to accumulate there.

It should be observed that a most important benefit of this scheme, which may, to some, appear almost futile-setting aside less than 5s.

towards a weekly debit of over £2-is that it has the advantage of preventing oversight of the need for this fund. Such neglect is the root of the troubles of so many hauliers who are new to the business. It is well worth while if on that account alone.

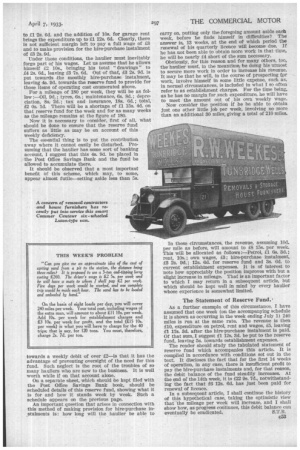

On a separate sheet, which should be kept filed with the Post Office Savings Bank book, should be scheduled details of this reserve fund, showing what it is for and how it stands week by week. Such a schedule appears on the previous page. An important question that arises in connection with this method of making provision for hire-purchase instalments is: how long will the haulier be able to carry on, putting only the foregoing amount aside each week, before he finds himself in difficulties? The answer is, 13 weeks, at the end of which period the renewal of his quarterly licence will become due. If he has not been able to obtain more work in that time, he will be nearly 1,4 short of the sum necessary.

Obviously, for this reason and for many others, too, the haulier must, in the meantime, be doing his utmost to secure more work in order to increase his revenue. It may be that he will, in the course of prospecting for work, involve himself in some little expense, such as, in normal circumstances, is included in what I so often refer to as establishment charges. For the time being, as he has no margin for such expenditure, he will have to meet the amount out of , his own weekly wage.

Now consider the position if he be able to obtain just one other little job per week, involving no more than an additional 30 miles, giving a total of 210 miles.

In these circumstances, the revenue, assuming 104. per mile as before, will amount to £8 15s. per week. This will be allocated as follows :-Petrol, £1 6s. 3d.; rent, 108.; own wages, £3; hire-purchase instalment, £3 2s. 94,; 12s. 6d. for reserve fund and 3s. 6d. to current establishinent expenses. It is of interest to note how appreciably the position improves with but a slight increase in mileage. That is an important factor to which I may return in a subsequent article, but which should be kept well in mind by every haulier whose experience is somewhat limited.

The Statement of Reserve Fund.,

As a further example of this circumstance, I have assumed that one week (on the accompanying schedule it is shown as occurring in the week ending July 1) 240 miles is run at the same rate. The revenue is then 110, expenditure on petrol, rent and wages, £5, leaving 11 17s. 3d. after the hire-purchase instalment is paid. Of that sum, I suggest £1 12s. 3d. be put to the reserve fund, leaving 55. towards establishment expenses.

The reader should study the tabulated statement of reserve fund which accompanies this article. It is compiled in accordance with conditions set out in the text. It discloses the fact that for the first 14 weeks of operation, in any case, there is insufficient profit to pay the hire-purchase instalments and, for that reason, the debit balance of the fund steadily increases. At the end or the 14th week, it is £22 9s. 74., notwithstanding the fact that 16 12s. 6d. has just been paid for renewal of licence.

In a subsequent article, I shall continue the history of this hypothetical case, taking the optimistic view that the mileage per week will increase, and I shall show how, as progress continues, this debit balance can eventually be eradicated. S.T.R.