1

1 2

2 3

3 4

4 5

5 6

6 7

7 8

8 9

9 10

10 11

11 12

12 13

13 14

14 15

15 16

16 17

17 18

18 19

19 20

20 21

21 22

22 23

23 24

24 25

25 26

26 27

27 28

28 29

29 30

30 31

31 32

32 33

33 34

34 35

35 36

36 37

37 38

38 39

39 40

40 41

41 42

42 43

43 44

44 45

45 46

46 47

47 48

48 49

49 50

50 51

51 52

52 53

53 54

54 55

55 56

56 57

57 58

58 59

59 60

60 61

61 62

62 63

63 64

64 65

65 66

66 67

67 68

68 69

69 70

70 71

71 72

72 73

73 74

74 75

75 76

76 77

77 78

78 79

79 80

80 81

81 82

82 83

83 84

84 85

85 86

86 87

87 88

88 89

89 90

90 91

91 92

92 93

93 94

94 95

95 96

96 97

97 98

98 99

99 100

100 101

101 102

102 103

103 104

104 105

105 106

106 107

107 108

108 109

109 110

110 111

111 112

112 113

113 114

114 115

115 116

116 117

117 118

118 119

119 120

120 121

121 122

122 123

123 124

124 125

125 126

126 127

127 128

128 129

129 130

130 131

131 132

132 133

133 134

134 135

135 136

136 137

137 138

138 139

139 140

140 141

141 142

142 143

143 144

144 145

145 146

146 147

147 148

148 149

149 150

150 151

151 152

152 153

153 154

154 155

155 156

156 157

157 158

158 159

159 160

160 161

161 162

162 163

163 164

164 165

165 166

166 167

167 168

168 169

169 170

170 171

171 172

172 173

173 174

174 175

175 176

176 177

177 178

178 179

179 180

180 181

181 182

182 183

183 184

184 185

185 186

186 187

187 188

188 189

189 190

190 191

191 192

192 193

193 194

194 195

195 196

196 197

197 198

198 199

199 200

200 201

201 202

202 203

203 204

204 205

205 206

206 207

207 208

208 209

209 210

210 211

211 212

212 213

213 214

214 215

215 216

216 217

217 218

218 219

219 220

220 221

221 222

222 223

223 224

224 225

225 226

226 227

227 228

228 229

229 230

230 231

231 232

232 233

233 234

234 235

235 236

236 237

237 238

238 239

239 240

240 241

241 242

242 243

243 244

244 245

245 246

246 247

247 248

248 249

249 250

250 251

251 252

252 253

253 254

254 255

255 256

256 257

257 258

258 259

259 260

260 Planning for Profit TYRE COSTING

Page 106

Page 107

If you've noticed an error in this article please click here to report it so we can fix it.

IS WORTHWHILE

THERE are wide variations in the life obtained from a set of tyres. The transport manager of a large fleet of staff cars and service vans tells me he obtains between 30,000 and 40,000 miles per set. This is about twice the distance many users can claim.. Admittedly, the manager in question operates his vehicles almost exclusively in agricultural areas. but the main reason for this high mileage is an efficient system of tyre maintenance and recording.

Bus companies achieve exceptional tyre mileages by similar means. It helps, of course, that they are sufficiently large to be able to employ staff exclusively for tyre-fitting. In many eases such staff are, in fact, employees of the tyre manufacturing company. The tyres fitted to the vehicle also remain

,the property of the manufacturer and payment is made on a mileage basis.

Smaller operators can reduce tyre costs if they adopt similar methods in their own servicing operations..

In recent years, increasing mileages have been achieved by improvement in tyre construction generally, Paradoxically, this advance could mean that any premature tyre failure resulted in a greater loss to the user. If formerly he were averaging 30,000 miles per tyre and had to discard one prematurely after 75 per cent. of its normal life, the loss in terms of mileage would be 22,500. But if the average mileage life were subsequently increased to 40,000, the loss would be increased to 30,000.

Reference to " The Commercial Motor' Tables of Operating Costs" confirms. that tyres represent a substantial proportion of the total operating cost of a commercial vehicle. For example, a. 7-ton petrol-engined rigid averaging 600 miles per week is shown to have a tyre cost per mile of I.60d.,—a total of £4. But because tyre costs • come within the category of deferred costs, the amount involved can easily be underestimated orignored if proper records are not kept.

Similarly, in terms of initial outlay,

rI2 replacement of a set of tyres can present a major problem to a small operator unless a sinking fund has been set up for that purpose immediately a new vehicle is put on the road. A 5-cwt. van would have tyres costing around £30 and the cost for larger vehicles would be: 7-tanner, 1200, 10-ton "attic.", £275, and a 16-ton eight-wheeled rigid around £450. With such large amounts the initial clerical work involved in setting up a tyre record system is fully justified. To inaugurate such a system, it is first necessary to record the rnanu• facturers' serial number which is branded on each cover.

The work involved in taking such an inventory, is Probably one of the main reasons so many operators do not keep individual tyre records. Yet the reduction in subsequent operating costs fully justifies the effort. Moreover, once this' initial work has been done, the daily work involved in both maintenance and recording is comparatively limited.

Readers often inquire why it is not possible to record the running cost of a set of tyres, rather than individual covers. The answer is that this apparent simplification would, in fact, complicate the issue, and also introduce inaccuracies in individual vehicle operating costs. With the exception of the one-vehicle fleet, tyres will be interchanged between the several vehicles in a fleet as well as between stock. Any attempt to keep track of an original set of tyres on any one vehicle would prove impracticable. In addition, any attempt to record the costs of .specific tyres against any one vehicle would result in gross underor over-charging among the several vehicles of the fleet.

The tyre stocks maintained by an average-size fleet user would probably include three types of cover, namely, new, re-treaded and part-worn. It would, therefore, belargely accidental whether a new. re-treaded or part-worn tyre were fitted in any particular instance, but there would obviously be a substantial difference in the actual cost. To provide a fair allocation of tyre costs, it is necessary to record these individually in respect of each cover, and to proportion the total cost according to the actual mileage logged against each vehicle.

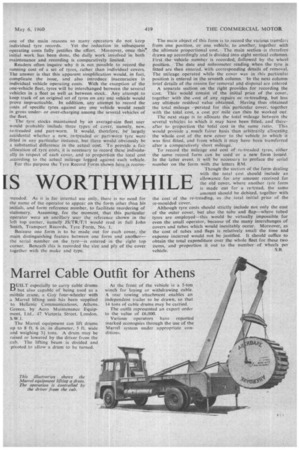

For this purpose the Tyre Record Form shown here is rccom mended: As it is for internal use only, 'there is no need for the name of the operator to appear on the form other than his initials, and form reference number, to facilitate reordering of stationery. Assuming, for the moment, that this particular operator were an ancillary user the reference shown in the left top corner, namely IS/TR/T/1 would read in full John Smith, Transport Records, Tyre Form, No. 1.

Because one form is to be made out for each cover, the main distinguishing feature between one form and another— the serial number on the tyre—is entered in the right top corner. Beneath this is recorded the size and ply of the cover together with the make and type. The main object of this form is to record the various transfers from one position, or one vehicle, to another, together with the ,ultimate proportional cost. The main section. is therefore drawn up accordingly and is divided into eight vertical columns. First the vehicle number is recorded, followed by the wheel position. The date and mileometer reading when the tyre is fitted are then entered, with corresponding details of removal. The mileage operated while the cover was in this .particular position is entered in the seventh column. In the next column brief details of the reason for removal and disposal are entered A separate section on the rightprovides for recording the cast. This would consist of the initial price of the cover, together with the cost of any _repairs or re-treading, but less any ultimate residual value obtained. Having thus obtained the total mileage %?perated for this particular cover, together with the total Cost, a cost per mile can then be worked out.

The next stage is to allocate the total mileage between the several vehicles to which it may have been fitted; and thereafter. to proportion the total cost In the same ratio. This would provide a much fairer basis than arbitrarily allocating the whole cost of the new cover to the vehicle to which it was first fitted, and from which it may have been transferred after a comparatively short mileage.

To record the mileage and coSt of re-treaded tyres, either. the same record form can be used or a new form issued. In the latter event, it will he necessary to preface the serial• number on the form with the letters RM.

Though the section of the form dealing with the total cost. shouldinclude an allowance for any amount received for the old cover, where another tyro form is made out for a re-tread, the same amount should be debited, together with the cost of the re-treading, as the .total initial price of the re-moulded cover.

Although tyre costs should strictly include not only the cost of the outer cover, but also the tube and flap—where tubed tyres are employed—this would be virtually impossible for even the small operator, because of the many interchanges of covers and tubes which would inevitably occur. Moreover, as the cost of tubes and flaps is relatively small the time and expense incurred would not be justified. It should suffice to obtain the total expenditure over the whole fleet for these two items, and proportion it. out to the number of wheels per vehicle. S.B.