Proper Organization Pa) in Keeping Costs

Page 32

Page 33

If you've noticed an error in this article please click here to report it so we can fix it.

One Man's Ideas of How to Keep Costs and Details of the Forms that he Uses and the Information that is Readily Available from Them

I T is always of considerable interest to discuss examples of cost recording because every operator, no matter what his system may be, is aware that it may quite possibly be open to criticism and he is always glad to learn how the other fellow keeps his records.

It is with that object in view that I put forward for discussion this week the accompanying series of forms_ They are unlike any that I have seen before and have certain points of interest to which attention may usefully be directed.

The operator who has sent them to me for criticism and comment has a fleet of 24 vehicles of various sizes.

He is interested more particularly in his total cost per annum, as his business is of such a nature that the most useful information he can have is that giving total cost per ton carried. He can arrive at that most effectively by ascertaining the total cost of operating a vehicle over a period and dividing that cost by the tonnage.

He has not, however—and this is my first comment— fallen into the mistake, so common in those circum stances, of assuming that it will be sufficient for his purpose if he makes a note of all that is spent on the whole fleet, thus obtaining the essential figure for total cost of transport.

He has realized that to ensure efficient operation it is necessary to know what each vehicle is costing day by day, week by week and month by month, so that a check is possible on sources of waste and extravagance and the merits of individual vehicles can be tested.

This operator, however, had gone a little farther. He has evidently appreciated that this careful check and comparison is, in ordinary circumstances, requisite in respect only of certain items. These, in order of importance, are : petrol consumption, oil consumption, main tenance cost and tyres. For these items he has separate sheets and keeps a more or less close check, depending upon the item concerned. For example, it should be fairly obvious that of the four the closest check must be kept upon petrol consumption.

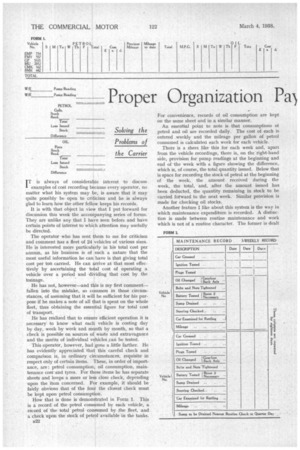

How that is done is demonstrated in Form 1. This is a record of the petrol consumed by each vehicle, a record of the total petrol consumed by he fleet, and a check upon the stock of petrol available in the tanks. B22 For convenience, records of oil consumption are kept on the same sheet and in a similar manner.

An essential point to note is that consumptions of petrol and oil are recorded daily. The cost of each is entered weekly and the mileage per gallon of petrol consumed is calculated each week for each vehicle.

There is a sheet like this for each week and, apart from the vehicle recordings, there is, on the right-hand side, provision for pump readings at the beginning and end of the week with a figure showing the difference, which is, of course, the total quantity issued. Below that is space for recording the stock of petrol at the beginning of the week, the amount received during the week, the total, and, after the amount issued has been deducted, the quantity remaining in stock to be carried forward to the next week. Similar provision is made for checking oil stocks.

Another feature I like about this system is the way in which maintenance expenditure is recorded. A distinction is made between routine maintenance and work which is not of a routine character. The former is dealt

with on Form 2. This provides for records covering three weeks and relating to two vehicles.

It should be noted that there are ten of these principal routine operations and most of them are required to be done within the period named. A Tine completely blank from end to end would suggest, therefore, that there had been some neglect and that the particular operation cited at the beginning of that line should be carried out immediately. The exception to this rule is indicated by the note at the bottom of the sheet: "Sump to be drained nearest routine check to quarter day."

It will be observed that there is no provision for any entry of cost relating to this work. I understand that the total mechanics' time hooked to this class of work is treated as a standing charge and spread evenly over the whole fleet.

This course is one which may be open to criticism, but probably it is satisfactory in the majority of cases. At least, it does ensure the observation of what is so often overlooked, i.e., that these routine maintenance operations do cost money and must be included in the item " mai ntenance. "

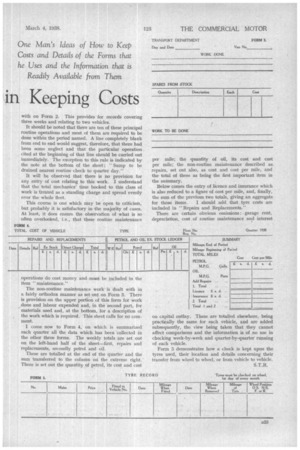

The non-routine maintenance work is dealt with in a fairly orthodox manner as set out on Form 3. There is provision on the upper portion of this form for work done and labour expended and, in the second part, for materials used and, at the bottom, for a description of the work which is required. This sheet calls for no corn • merit.

I come now to Form 4, on which is summarized each quarter all...the data which has been 'collected in the other three forms. The weekly totals are set out on the left-hand half of the sheet—first, repairs and replacements, secondly petrol and oil.

These are totalled at the end of the quarter and the sum transferred to the column on the extreme right.' There is set out the quantity. of petrol, its cost and cost

per mile; the quantity of oil, its cost and cost per mile; the non-routine maintenance described as repairs, set out also, as cost and cost per mile, and the total of these as being the first important item in the summary.

Below comes the entry of licence and insurance which is also reduced to a figure of cost per mile, and, finally, the sum of the previous two totals, giving an aggregate for those items. I should add that tyre costs are included in " Repairs and Replacements."

There are certain obvious omissions: garage rent, depreciation, cost of routine maintenance and interest on capital outlay. These are totalled elsewhere, being practically the same for each vehicle, and are added subsequently, the view being taken that they cannot affect comparisons and the information is of no use in checking week-by-week and quarter-by-quarter running of each vehicle.

Form 5 demonstrates how a check is kept upon the tyres used, their location and details concerning their transfer from wheel to wheel, or from vehicle to vehicle. S.T.R.