Recording Tyre Costs

Page 73

Page 74

If you've noticed an error in this article please click here to report it so we can fix it.

IN the latest edition of The Commercial Motor Tables of Operating Costs, a tyre cost per mile of 1-49d. is . given for an oil-engined 7-tonner, compared with a total running cost per mile of 9.63d. When averaging 800 miles a week, the corresponding tyre cost per week would be £4 19s. 4.d. as against a total running cost of £32 2s. Od. This one item of equipment is therefore more than a sixth of the total running cost. On this score alone it justifies particular attention, both as regards routine maintenance and systematic recording.

As a result of continuing improvements during post-war years in both design and construction, tyre manufacturers have provided transport users with equipment capable of achieving appreciably higher mileages than previously. It is therefore especially important that operators should take advantage of this potentially higher mileage by careful attention to tyres generally. In this respect it is pertinent to note that premature failure of a tyre will now, in all probability, result in a greater loss, in terms of mileage, than would have previously been the case.

For many years the larger operating companies have been fully aware of the advantages to be obtained from regular attention to tyre maintenance and recording, but in the main this does not apply to the smaller user. Especially when such operators put new vehicles into service, there may appear to be no urgent reason to set up a tyre recording system, nor even to make financial provision for the time when replacement of tyres will be necessary. In the example just quoted, the tyre cost per week of £4 19s. 4d. for the 7-ton oiler would soon add up to an appreciable sum after the first few months of operation.

As with other items of deferred expenditure, such as major overhaul and the ultimate replacement of the vehicle itself, the prudent procedure would be to set up a sinking fund to which amounts appropriate to the weekly estimates of costs would be transferred until such time as actual expenditure was incurred. Otherwise a sum of £186—which is the cost for a set of tyres taken as representative for the 7-tonner just mentioned—may not be readily available when replacement becomes inevitable.

THE reluctance shown by many small users to install a tyre recording system stems largely from an omission to take proper steps at the outset, and later to be unable to allocate the time both to inaugurate such a scheme and to catch up on arrears of records. It must be admitted thatinitially a substantial amount of work will be necessary in

recording the serial number of every tyre fitted to the fleet.

Because, with most fleets, it will be rare for all vehicles to be in the depot at the same time, such an inventory would probably have to be taken either overnight or during a week-end in the case of vehicles engaged on long-distance work.

Once this inventory has been taken, however, subsequent tyre recordings will be both simple and limited, occurring only when a tyre change is made or a new vehicle acquired. In relation to vehicle cost recording generally, it has been repeatedly recommended in this series of articles that the basis of such recordings should be individual vehicles. It is natural, therefore, that those not familiar with tyre recording should continue to think in terms of the total tyre equipment of a vehicle. Although this would seem a logical approach, in practice it very soon becomes impossible to continue to record the cost of tyres—as a set--• throughout their life because even in the smallest fleet there will

usually be substantial interchange of tyres between one vehicle and another.

Even if it were assumed that the cost of these several interchanges would ultimately balance out so that the full cost of the original set of tyres could be considered to be a charge on that vehicle, substantial overand undercharging for tyres among the several vehicles of the fleet would result.

IN any established fleet the total tyre stocks at any time could be loosely divided into three categories—namely, new, part-worn and possibly retreaded, where such a policy was adopted. In those fleets where it was the custom for vehicles to carry spare tyres and a change was made by a driver .whilst out on the rOad, it should be common practice for him to hand in the defective tyre on his return to depot.

The type of replacement he then received would in many instances be dependent .upon the level of stocks at that mo:nent. • As a result he could receive either a new, part-worn or retreaded tyre, and whilst this would be largely a matter of chance, the difference in cost if allocated solely to that vehicle would be substantial. It will also be readily apparent that it would be virtually impossible to keep track of the sets of tyres fitted as original equipment as separate entities.

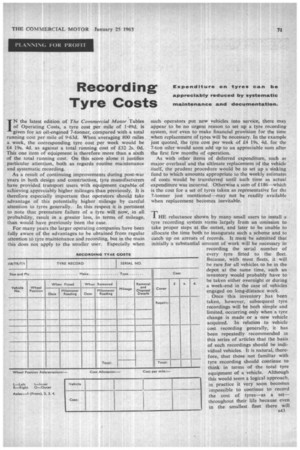

It is for this reason that the Tyre Record Form recommended here relates to individual tyres. As with forms previously recommended in this series, it is intended for internal use only and there is, therefore, no need for the name of the operator to appear on the form. All that is necessary are possibly his initials and a reference number to facilitate reordering of stationery. As an example, it is here assumed that the name of the operator is Arthur Brown and that the reference number shown here, namely AB/TR/T/1, infers "Transport Record Tyre Form No. 1 ".

As already stated, one form is to be used for each cover and therefore it is important that the main distinguishing feature as between one form and another—the serial number which is moulded on to each cover—should be entered in the right top corner. Immediately beneath this should be recorded the size and ply rating of the cover, as well as the make and type.

THE principal purpose of this form is to facilitate the recording of the various transfers of each cover either from one position to another on the same vehicle or, alternatively, from one vehicle to another. At the same time, the several mileages in the various positions are also recorded, so that it is possible to determine accurately the ultimate proportional cost.

Accordingly, the main section of the form is divided into eight vertical columns. In the first column the vehicle number is recorded, followed by the wheel position in which the cover is fitted. Then follow the date and mileometer reading when the cover is fitted, with corresponding details as to when it is removed to another vehicle or transferred to a different position on the same vehicle.

It is then possible to calculate the mileage operated whilst the cover was in any particular position, and this is entered in the seventh column. There then follow details of the reason for removal, or possibly disposal, in the next column of the table. .

• 944

On the right of the form a separate section is provided to record the total cost of each cover throughout its working life. This would include not only the initial price of the cover, but also the cost of any repairs and retreading if, in fact, it were the policy of the operator to do this. From this total would then be deducted any residual value which was ultimately obtained. Because the total mileage run for each particular cover has been recorded, it is then . possible, by a, division of the total cost by this figure, to obtain a cost per mile.

Having obtained this cost per mile, the operator is then able to make a fair allocation of the total cost as between the several vehicles to which the cover may have been fitted. This final calculation is, of course, the whole purpose of the form. It provides a far sounder basis than allocating the whole cost of a new cover to whatever vehicle it happens to be fitted in the first instance.

When it is the policy of the operator to use retreaded tyres, two alternative methods of recording their use can be employed. Assuming the serial number remains the same after retreading has taken place, the originaL Tyre Record Form made out for the new cover can continue to be used. Alternatively, another form can be issued, in which case it might be helpful to preface the serial number with such letters as RM (i.e., remould) to facilitate identification.

WHEN dealing with the section of the form in which the total cost of the cover was recorded, it was stated that an allowance should be made for any amount received by the sale of the old cover. When, however, it is the policy of the operator to retread tyres and, in addition, to issue separate Tyre Record Forms for the retreaded covers, the same amount which was deducted from the total cost of the new cover would then be debited, together with cost of retreading, as the total initial price of the remoulded cover.

It will have been noted that use has been made of both the word " tyre " and "cover ". It must be admitted that when dealing with tyre costs these should include not only the cost of the cover, but also the tube and flap, assuming, of course, that tubed tyres are, in fact, fitted. As with several other aspects of transport recording and costing, however, some allowance has to be made in the interests of simplicity. Relative to the cost involved, it would be impractical for the operator of even a small fleet to record the many interchanges of covers and tubes which occur, Even if this were achieved, the ultimate proportion of cost would be so small that the expense in terms of time involved could seldom be justified by such action.

Strictly speaking, therefore, a.Tyre Record Form relates to the movement of a cover only, but by common usage the former description is generally accepted. As some provision, however, has to be made for the total expenditure on tubes and flaps throughout the fleet, it would be convenient, and probably sufficiently accurate for the purpose, to proportion this relative to the number of wheels per vehicle, assuming that there was not too wide a range of vehicles being operated.