A game of two halves

Page 10

Page 11

Page 12

Page 13

If you've noticed an error in this article please click here to report it so we can fix it.

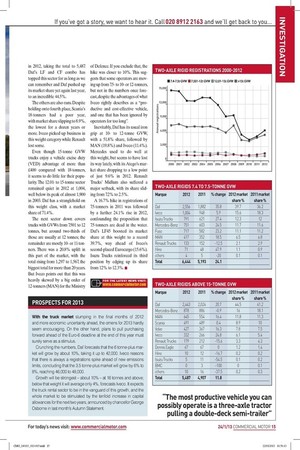

New truck sales activity in 2012 showed two different patterns in the first half of the year and the second Words: David Wilcox DURING THE FIRST half of 2012, registrations of new trucks over 3.5-tonne GVW surged ahead, and by the end of June were 26% up on 2011's first-half total, according to data from the Society of Motor Manufacturers and Traders (SMMT). But the market stalled in the second half, turning sharply downwards in the final quarter. The net result of this registrations rollercoaster was a total of 45,702 new trucks in 2012, only 6.4% higher than the 2011 figure.

Although an uplift of 6.4% is gratifying, this is measured against what was a fairly weak performance in 2011. In fact, the 2012 truck market was 10% smaller than the average of the previous dozen years (2000-2011).

The "proper" truck market, covering trucks of 6-tonne GVW grew by just 3.1% last year, up from 37,410 to 38,576. Last year, market leader Daf forecast a rise of around 5%, while the SMMT expected a "broadly flat year': Market share Our charts showing manufacturers' share of the 6 tonnes-plus market highlight Daf's dominance in 2012. Its 28.9% share is second only to the 29.8% it held in 2009 when Daf did not cut production as sharply as other manufacturers during that year's economic downturn, and so had trucks to sell at bargain prices. Daf's core strength is two-axle rigids, where its LF and CF ranges captured no less than 43.4% of the market in 2012.

In contrast, second-placed Mercedes-Benz is stronger in the tractor sector, where it edged ahead of Daf last year with 20.4% to Daf's 19.9%. Mercedes' overall share of the 6 tonnes-plus market slipped back just a tad last year, from 16.9% to 16.7%. Then come MAN, Scania and Volvo, locked in battle and swapping positions for the last decade, each with a market share of between 10% and 13%. Scania leap-frogged its two rivals in 2012, claiming 12.1%, ahead of MAN's 11.2% (down from 12.8%) and Volvo's 10.3%. Down from 12.4% in 2011, this is Volvo's lowest market share for more than 15 years and the sharpest downturn of the big seven truck brands.

Iveco's share of the 6 tonnes-plus market has been tracking steadily downwards, from 15.4% in 2002 to 7.6% in 2011. The efforts of Iveco's reinvigorated UK management tors will continue to move to threereduction of almost 40% in registrations of two-axle Mercedes units. Scania's tractor market share crashed in 2011, taking it from second to fifth, but it bounced back last year with registrations up 23.4%, taking Scania back up to third.

Volvo's aforementioned market slippage in 2012 can be traced back to a 23.3% drop in its tractor unit numbers, far worse than the sector's decline of 7.2%. Only MAN's tractor count fell further, down 27%. As with Volvo, it is this sharp drop in tractor business that is behind MAN's loss of overall truck market share in 2012.

Iveco takes the "most improved" prize, growing Stralis registrations by 46.7% to take its tractor market share up from 2.3% to 3.6%. Iveco UK MD Luca Sra had promised a renewed assault on this sector - it seems to have paid dividends. Surprisingly, fuel-efficient EcoStralis models accounted for only 12% of all new Stralis 6x2 units last year.

Multi-axle rigids Overall growth of 10.2% in the number of multiwheelers masks a modest 4.5% uplift in the threeaxle sector (from 3,994 to 4,172) and a far healthier 22.5% increase in the number of four-axle chassis (from 1,850 to 2,267). The latter marks the gradual recovery in the construction market and pent-up demand for fleet renewal. Nevertheless, it still leaves the 8x4 sector well down on its long-term average of around 3,000 a year before the crash of 2009.

More than 80% of all the threeaxle rigids are 6x2 chassis (as opposed to 6x4) and about 25% (around 850) of the 6x2s are refuse collection vehicles, namely Mercedes Econic and Dennis Eagle. That leaves around 2,500 of these 6x2 chassis bought for tankers and general distribution duties in 2012. A 56% rise in the number of 6x2 chassis in 2011 was reckoned to be driven by operators switching from 18 tonnes on two axles to 26 tonnes on three, in search of distribution productivity.

There is nothing in the 2012 data to suggest this trend has continued to track upwards.

The combination of Econic and Axor made Mercedes top dog in the three-axle sector in 2012, with 22.1% market share, ahead of Daf (18%) and Dennis Eagle (15.7%). This was also a rare bright spot for Renault, with registrations up by 79.8% to take its share up to 5.3%.

Among four-axle rigids it is Scania that rules the roost with a 26.4% share, just ahead of Volvo (24.3%) and Daf (20.9%) MAN comes in fourth place at just 8.8%. The arrival of Mercedes' new Arocs construction chassis range clearly cannot come soon enough - the company's four-axle truck registrations slipped by 19.9%, taking market share down to a woeful 5.2%.

Two-axle rigids The sector labelled "two-axle rigids above 15-tonne GVVV" is really all about 18-tonners, which account for about 90% of this sector's total. It is a relatively stable market, invariably accounting for 18% to 21% of all rigid trucks over 3.5-tonne GVVV. The number of 15 tonne-plus chassis rose by 11.8% in 2012, taking the total to 5,487 Daf's LF and CF combo has topped this sector for as long as we can remember and Daf pushed up its market share yet again last year, to an incredible 44.5%.

The others are also-rans. Despite holding onto fourth place, Scania's 18-tonners had a poor year, with market share slipping to 8.9%, the lowest for a dozen years or more. Iveco picked up business in this weight category while Renault lost some.

Even though 15-tonne GVW trucks enjoy a vehicle excise duty (VED) advantage of more than £400 compared with 18-tonners, it seems to do little for their popularity. The 12.01to 15-tonne sector remained quiet in 2012 at 1,004, well below its peak of almost 1,900 in 2003. Daf has a stranglehold on this weight class, with a market share of 71.4%.

The next sector down covers trucks with GVVVs from 7.501 to 12 tonnes, but around two-thirds of those are usually at 12 tonnes; the remainder are mostly 10or 11-tonners. There was a 20.8% uplift in this part of the market, with the total rising from 1,297 to 1,567 the biggest total for more than 20 years. But Iveco points out that this was heavily skewed by a big order of 12-tonners (MAN) for the Ministry of Defence. If you exclude that, the hike was closer to 10%. This suggests that some operators are moving up from 75to 10or 12-tonners, but not in the numbers once forecast, despite the advantages of what Iveco rightly describes as a "productive and cost-effective vehicle, and one that has been ignored by operators for too long".

Inevitably, Daf has its usual iron grip at 10to 12-tonne GVW, with a 51.8% share, followed by MAN (19.8%) and Iveco (11.4%). Mercedes used to do well at this weight, but seems to have lost its way lately, with its Atego's market share dropping to a low point of just 9.6% in 2012. Renault Trucks' Midlum also suffered a major setback, with its share sliding from 7.2% to 2.5%.

A 16.7% hike in registrations of 75-tonners in 2011 was followed by a further 24.1% rise in 2012, confounding the proposition that 75-tonners are dead in the water. Daf's LF45 boosted its market share at this weight to a record 39.7%, way ahead of Iveco's second-placed Eurocargo (15.6%). Isuzu Trucks reinforced its third position by edging up its share from 12% to 12.3%. • TRACTOR UNIT REGISTRATIONS Marque 2012 2011 % change 2012 market 2011 market share % share % Mercedes-Benz 3,481 3,559 -2.2 20.4 19.3 Daf 3,400 3,622 -6.1 19.9 19.7 Scania 3,056 2,476 23.4 17.9 13.4 Volvo 2,544 3,315 -23.3 14.9 18 MAN 2,195 3,005 -27 12.8 16.3 Renault Trucks 1,799 2,021 -11 10.5 11 Iveco 619 422 46.7 3.6 2.3 Nino 3 n/a Total 17,097 18,420 -7.2 MULTI-AXLE RIGIDS Marque 2012 2011 %change 2012 market 2011 market share% share% Daf 1,226 1,078 13.7 19 18.4 Scania 1,105 1,106 -0.1 17.2 18.9 Mercedes-Benz 1,041 917 13.5 16.2 15.7 Volvo 965 928 4 15 15.9 MAN 698 633 10.3 10.8 10.8 Dennis Eagle 681 597 14.1 10.6 10.2 Renault Trucks 390 274 42.3 6.1 4.7 Iveco 211 224 -5.8 3.3 3.8 Nino 114 80 42.5 1.8 1.4 others 8 7 14.3 0.1 0.1 Total 6,439 5,844 10.2 TWO-AXLE RIGIDS 7.4 TO 7.5-TONNE GVW Marque 2012 2011 % change 2012 market 2011 market share % share % Daf 2,556 1,882 35.8 39.7 36.2 Iveco 1,004 948 5.9 15.6 18.3 Isuzu Trucks 791 621 27.4 12.3 12 Mercedes-Benz 751 603 24.5 11.7 11.6 Fuso 717 582 23.2 11.1 11.2 MAN 417 352 18.5 6.5 6.8 Renault Trucks 133 152 -12.5 2.1 2.9 Nino 71 48 47.9 1.1 0.9 others 4 5 -20 0.1 0.1 Total 6,444 5,193 24.1 TWO-AXLE RIGIDS ABOVE 15-TONNE GVW Marque 2012 2011 % change 2012 market 2011 market share % share % Daf 2,443 2,024 20.7 44.5 41.2 Mercedes-Benz 878 886 -0.9 16 18.1 MAN 645 554 16.4 11.8 11.3 Scania 491 489 0.4 8.9 10 Volvo 427 367 16.3 7.8 7.5 Iveco 332 266 24.8 6.1 5.4 Renault Trucks 179 212 -15.6 3.3 4.3 Dennis Eagle 67 67 1.2 1.4 Nino 10 12 -16.7 0.2 0.2 Isuzu Trucks 5 11 -54.5 0.1 0.2 BMC 3 -100 0.1 others 10 16 -37.5 0.2 0.3 Total 5,487 4,907 11.8 PROSPECTS FOR 2013 With the truck market slumping in the final months of 2012 and more economic uncertainty ahead, the omens for 2013 hardly seem encouraging. On the other hand, plans to pull purchasing forward ahead of the Euro-6 deadline at the end of this year must surely serve as a stimulus.

Crunching the numbers, Daf forecasts that the 6 tonne-plus market will grow by about 10%, taking it up to 42,000. Iveco reasons that there is always a registrations spike ahead of new emissions limits, concluding that the 3.5 tonne-plus market will grow by 6% to 8%, reaching 46,000 to 48,000.

Growth will be strongest - about 10% - at 16 tonnes and above; below that weight it will average only 4%, forecasts Iveco. It expects the truck rental sector to be in the vanguard of this growth, and the whole market to be stimulated by the tenfold increase in capital allowances for the next two years, announced by chancellor George Osborne in last month's Autumn Statement.