Beware of Insurance Pitfalls

Page 50

Page 53

If you've noticed an error in this article please click here to report it so we can fix it.

The Cheapest is Not Alititys the Best. Trouble Awaits the Operator Who Places Insurance Business Badly and Neglects to Check his Policy

IN beginning an up-to-date article on insurance

I am compelled to repeat the hoary, but necessary, advice to all operators of commercial vehicles always to read the insurance policy carefully. Look for those items which are not covered, rather than those that are.

The necessity of giving this advice will be appreciated when I state that hardly a week pas:es but someone discovers that the insurance policy for which he has, perhaps, been paying

substantial annual premiums for many years, is not all that he thought it to be. Some essential requirement may have been overlooked and, as a result, an operator is involved in heavy expendi ture which he expected the insurance company to meet.

Particular care is necessary in selecting the company with which to do business. The opera

tor is naturally inclined to deal with the one which quotes the lowest premiums. He is not necessarily wrong if he makes that choice, but if he does so he should be especially careful in reading the policy. He should compare policies and price-; to discover what is being offered at the higher premiums to justify the increase,

Actually, the selection of a suitable company is difficult. It is almost as difficult as it is to choose the policy that will afford the widest cover at a reasonable premium. In my view, the best plan is to go to a reputable broker—one who is accustomed to the insurance of heavy motor vehicles and is familiar with the other insurances that are involved in the operation of commercial vehicles. Place the business in his hands and ask his advice, In that way the user not only secures expert assistance, hut puts himself in a position to be able to make use of the broker's experience when claims are contested or when conditions arise which involve disputes as to liability.

In the latter respect, it should be appreciated that an insurance broker of standing is a man with plenty of business. He places his business with a large number of insurance companies which are glad to obtain it and will therefore put themselves out to please him. He is in a position to bring pressure to bear upon the insurance companies. This is rarely so in the case of the ordinary vehicle owner, especially the small man with only one or two vehicles.

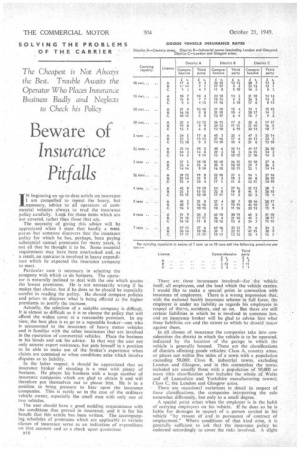

The user should have a good nodding acquaintance with the conditions that prevail in insurance, and it is for his benefit that this article has been written. The accompanying schedules of premiums which are applicable to various classes of insurance serve as an indication of expenditure on that account and as a check upon quotations 1816

There are three imurances involved—for the vehicle itself, all employees, and the load which the vehicle carries. I would like to make a special point in connection with insurance of employees. There is a wrong impression that, with the national health insurance scheme in full force, the employer is under no liability as regards his employees in respect of iltnss, accidents, and so on. But there are still certain liabilities in which he is involved in common law, and an insurance broker will be glad to advise him what these liabilities are and the extent•to which he should insure against them.

In all classes of insurance the companies take into consideration the district in which the vehicle is to be operated, indicated by the location of the garage in which the vehicle is generally housed. These are the classifications of districts affecting goods vehicles: Class A, country areas, or places not within five miles of a town with a population exceeding 50,000; Class B, industrial towns, excluding London and Glasgow, and in this connection the towns included are usually those with a population of 50,000 or more (this classification also includes the whole of Wales and all Lancashire and Yorkshire manufacturing towns); Class C, the London and Glasgow areas.

There are occasional variations in detail in respect of these classifications, the companies interpreting the rule somewhat differently, but only to a small degree.

A special point arise; when the employer is in the habit of carrying employees on his vehicle. If he does so he is liable for damages in respect of a person carried in his vehicle "by reason of and in pursuance of contract of employment." Where conditions of that kind arise, it is generally sufficient to 'ask that the insurance policy be endorsed accordingly to cover the risks involved. A slight addition to the premium may be asked on account of that endorsement, but that is not the invariable rule.

The classifications and the conditions under which passenger vehicles are insured are much more complicated than than already set out, which apply to goods vehicles. The simplest way to deal with them is to take the three tables of premiums for passenger vehicles one by one,. Table I applies to those vehicles which do not come under the conditions • of insurance of passenger vehicles in • Tables IT and Ill. So far as I can ascertain, Table I covers coaches used solely for private hire. The rates are as follows:— (a) Where the Road Traffic Acts, 1930-1934, apply to:—

(i) Public service vehiclesused as contract carriages, and express carriages restricted to excursions and tours.

(ii) Public service vehicles used as stage or express carriages on services restricted to the conveyance of workpeople of a specified company or number of companies to and from their places of employment.

(iii) Public service vehicles that do not enter the London area, and are used as stage or express carriages, but without the picking-up of passengers en route at less than the fare for the full journey.

(b) Vehicles in Northern Ireland and other areas engaged on private hire (the Isle of Man is excluded here).

(c) Vehicles in the Isle of Man which do not run to a set timetable and where no intermediate fare is charged, and vehicles in the Isle of Man which are let • out under contract at a fixed sum_ The rates are set out in Table

Now comes the third class, which applies as follows:— (a) .Where the Road Traffic Acts, 1930-1934, apply .to:— Vehicles engaged on stage or express services which do not come tinder the description above as applying to Table II.

(b) Vehicles.in Northern Ireland and other areas on public hire (the Isle of Man is excluded).

(c) Vehicles in the Isle of Man which run to a set timetable or where intermediate fares are charged.

There are some special provisions. First, vehicles which normally would be rated under Table III (a) may be rated according to Table II, provided that the 'average weekly mileage per vehicle under stage or express service licences does not exceed 250 and the routes authorized do not enter the London area. This applies only to vehicles garaged in district A. Vehicles otherwk,e rateable under Table Ill (al may be rated as in Table 11, plus 50per cent., provided that the services on which they operate are limited to not more than three named days per week, do not extend beyond a radius of 25 miles from the garage from which the vehicles operate, and do not enter the London area.

Districts A. B and C are similar to those given in respect of, goods vehicles, but there are certain restrictions laid downFirst, the district for rating purposes is the highest rated district which the vehicle enters. There is a special proviso applying to :Glasgow, for if a vehicle enters that area, each case is liable to be considered on its merits and a higher premium applied.

Policies may be extended without additional premium to indemnify against liability arising from the negligence of the insured party, his servants car any person issuing tickets to fare-paying passengers.

There are two classes which also call for special consideration: (a) Bus insurances 'Of municipalities, and (b) bus insurances covering tram andrailway undertakings.

It should be appreciated that the three tables of premiums are for insurance of the vehicle. Passenger risk must also be covered and the premium may be from 9s. to 10s. per 'seat, based upon the total passenger-seating capacity, plus any extra number carried b.y permission of the authorities.