WHAT ARE AIR PROFITS?

Page 46

Page 47

Page 48

If you've noticed an error in this article please click here to report it so we can fix it.

IAM often asked What, in my view, is a fair assessment of the percentage profit which a haulage tusiness should show. The calculation of the percentage, in a case like this, -should be based on the total cost. In other words, the total of standing charges, plus running costs and establishment costs, is to be taken as 100 per cent. and the net revenue in excess of that figure is the net profit which, if the above question is to be answered, must be set out as a percentage of that 100.

A profit of 20-25 per cent. is reasonable in the majority of cases, having in mind the risks which attach to most enterprises of this nature. The lower figure would apply in respect of steady, continuous work, and the -latter to operations which fluctuate rather widely, from seasonal or other Causes. This 'profit is obtainable, but it is not by any means the general experience of hauliers.

It appears to be, to some extent, a matter of opinion as to whether the figure is reasonable, or, rather, perhaps, it is not so much opinion as force of circumstances which decides. I have not met many hauliers who would refuse that percentage of profit, but I have found many who seem unable to obtain it. Some examples of what can and cannot be secured may be of interest.

Quite recently I was asked to assist in preparing a quotation for a contract of haulage. A careful assessment of the total costs demonstrated that about £3,000 per annum would meet them. I recommended an addition of 20 per cent., the work being steady and, therefore, justifying the acceptance of the lower ratio of profit. He cut my percentage in half, adding only 10 per cent., and quoted £3,300. The prospective customer told him that his price was over £1,000 in excess of what he anticipated paying!

Again, .discussing a tentative contract with a prominent London contractor, I suggested, after going into B32 the figures and considering the type of contract, that 15 per cent, would be a fair profit. He laughed at me and said that if he could obtain a margin of 5 per cent, on work, of that class he would be very pleased.

An examination of the causes in cases such as these is always interesting. The first of the above two was a quotation. by a contractor to take over, in its entirety, the road transport of an ancillary user. It was obvious that this

ancillary user, in assessing his own costs, was omitting some extensive contingent expenses involved in operating his own transport. It would not be fair for me to give details, as the work was confidential, but I can indicate my meaning by suggesting that he was entirely overlooking the value of the considerable portion portion of his premiseswhich he had to set apart for the housing and maintenance of his fleet.

The second case was definitely one of haying to meet persistent rate-cutting. It is well known that in the London area there are operators who are keen on contract-licence work, for reasons which, no doubt, will be obvious to the majority of my readers. They are content to work on this extremely narrow margin of profit if they can achieve their objective.

With the above conditions in mind, it seems a far cry to those days when hauliers were able to work on the basis of charging double the total vehicle operating costs. Even if it be taken that their establishment charges and contingent expenses—the latter probably heavy in those days—totalled 50 per cent, of their operating costs, there was still a margin of 35 per cent. as net profit.

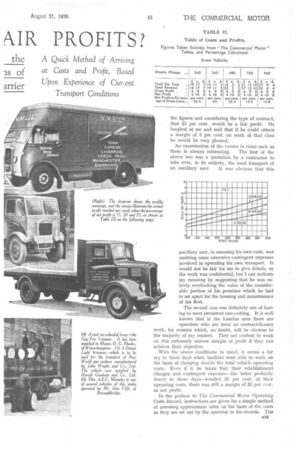

In the preface to The Commercial Motor Operating Costs Record, instructions are given for a simple method of assessing approximate rates on the basis of the costs as they are set out by the operator in his records. The method is to double the standing charges per week, that being assumed to be sufficient to cover all establishment costs and contingent expenses, and leave a reasonable margin of profit. Then, in order to make some slight allowance for mileage run, it is recommended that a small fraction of a penny be added to the ascertained running cost per mile. How this system works out is shown in Table I, in connection with the operation of

6-ton lorry over a: variety of mileages.

A .somewhat similar method is used in The Com-' rnercial Motor Tables of Operating Costs. Here, assumed figures for establishment costs are taken, along with an arbitrary figure for the profit per week, which, it is estimated, the haulier should expect to earn with particular types of vehicle, In these figures no provision is made for differentiation in mileage. What is intended is to give the haulier who has no idea of

profits some indication of his minimum charges. Table II shows, in a similar manner to Table I, how this method operates, again in connection with a 6-ton vehicle. It will be apparent that the net profit, calculated according to this method, is lower than the on above described and in the upper region of mileages, at any rate, is closer to actuality. Incidentally, it is in the upper region of mileages that vehicles of this type more usually operate, at least in the hands of hauliers.

A more rational method of estimating profit and corresponding chargeP is to take the profit as being most reasonably calculated as a percentaghi on outgoings. In Table 111, figures are set out in this manner, according to three different rates, namely, 15 per cent,, 20' per cent., and' 25 per cent. The -graphs (Figs., I and .II) illustrate the difference between these various methods.

Fig. I embodies the figures in Tables I and II. It is arranged to illustrate what the percentage profit is if it be calculated according to the above method, namely, taking operating costs, plus establishment charges, as a basis. Fig. II is arranged to show the actual profit per week reached when the percentage is 15, 20, and 25. S.T.R.