Deflating Tyre Costs

Page 64

Page 67

If you've noticed an error in this article please click here to report it so we can fix it.

TYRES may account for more than 10 per cent. of the -total cost. of operating a Commercial vehicle. To run a 5-ton oil-engined platform lorry .600 miles would cost approximately £32 I2s., the tyre 'cost being £3 10s. Moreover, unlike some aspects of operational efficiency, improvement in tyre Wear can be obtained by the application of comparatively simple techniques, provided they are allied to the important

element of persistence. .. • • Comparison of the initial price of a vehicle and the cost of a set of tyres 'emphasizes the importance of their care. Taking an average of the vehicles available on the British market, the 5-cwt. petrol-engined van, costing around £460, would have

.set of tyres worth about £30, whilst a 3-tonner priced at £1,000 would be shod-with tyres costing about 010.

In the range of vehicles of higher carrying capacities, tyre specification may vary .according to individual preferences. A maximum-load four-wheeled oiler priced at £3,500 may have tyres costing more than £300. At the top end of the scale,. the tyres of an eight-wheeler could cost over £500.

Clear Indication Converting the cost of a' set of tyres to a cost per mile, as required when calculating the five items of running costs, gives a clear indication of the economies that can be achieved by improved maintenance methods. With the 5-cwt. van the cost per mile would be 0.36d., where mileage life averaged 20,000, and 0.24d. at 30,000 miles. At £110 per set, the cost per mile drops from 0.88d. at 30,000 miles to 0.66d. at 40,000 miles. A multi-wheeler, with tyres valued at £500, would have a tyre costper mile of 3d., again at 40,000 miles per set.

All these castings presuppose, of course, that detailed records are kept. These are essential for two' reasons-. They indicate, in the first place, where excessive wear is being experienced and, after remedial action has been taken, whether the desired results have been achieved.

It must be admitted, however, that initially the introduction'of a tyre-record system for .an existing fleet does necessitate extra work, particularly if the fleet is large. It involves recording the manufacturer's serial number branded on each cover, and as nearly as possible simultaneously throughout the fleet, to

avoid either duplication or omission. Thereafter, the actual day-to-day maintenance of the system is comparatively simple, as records arc taken only when tyre changes are made or new vehicles are introduced into the fleet.

The amount of work involved in inaugurating such a system is undoubtedly the nason why so many. operators do not keep track of their tyre costs other than in totalif at all. Yet the proportion of total operating costs represented by tyres more than justifies the effort.

Natural Corollary .

Where an overall costing system has been set up with the prime objective of ultimately obtaining an operating cost per vehicle-mile, it would appear a natural corollary to record the cost per mile of each set of tyres, rather than of every cover. The owner-driver may well insist that, barring accidents, the original set of tyres may well remain on the vehicle for a long time, albeit in different positions at later stages. Where more than one vehicle is operated, however, tyres will be interchanged between vehicles and stock, and any attempt to record the original set of tyres as an entity until disposal of that particular vehicle must eventually break down.

Incorrect allocation of tyre costs per vehicle can also occur if individual tyrr; records are not kept For example, it is not unusual for fleet users' stocks of spare tyres to include \three classes of cover—new, retreaded or part-worn. When it becomes necessary to match up a twin, or a combination of tyres on a multi-wheeled vehicle, for example, it may well be that the precise c-ist of the replacement is either not available or could not he fairly charged to any particular vehicle. The only way in which tyre costs can be fairly apportioned is to record the mileage actually logged by each cover and allocate costs according to actual usage.

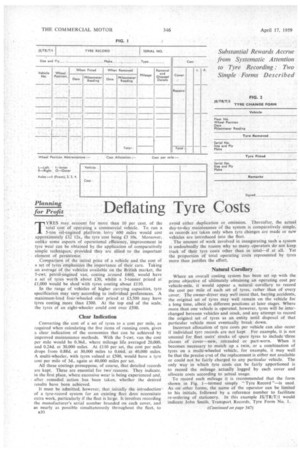

To record such mileage it is recommended that the form shown in Fig. 1.—termed simply "Tyre Record "—is used. As on other forms, the name of the operator can be limited to his initials, followed by a reference number to facilitate re-ordering of stationery. In this example JS/TR/T/1 would indicate John Smith, Transport Records, Tyre Form No. I.

Because one record is to be-made out for each' tyre the distinguishing feature between one form and another—the serial letters and numbers branded on every cover—is given prominence at the right top corner, Following this are detailed the size, ply, rating, make and type.

The main section of the form is drawn up to facilitate the recording of whatever positional or vehicle changes are made throughout the life of the cover. In the first column is shown the number of the vehicle to which the , cover is at present fitted, followed by the wheel position. Then the date and mileometer reading when fitted are recorded, and similarly when removed. The mileage done while the cover is fitted to each vehicle can thus be obtained. Brief dettils as to the reason for removal and disposal, as applicable, are also noted.

A subsection of the form permits the entry of cost data, including not only the original price of the cover, but also the cost of repairs en remoulding. horn the resulting totals of cost and mileage, a cost per mile for that particular cover can be obtained. The allocation of the total between various vehicles on which it was used can then be calculated more equitably than by arbitrarily charging the cost of each new tyre to whatever vehicle it might originally have been fitted, regardless of the mileage it may actually have run on that vehicle.

Where substantial use is made of retreaded tyres, two alternative methods of recording are possible, Assuming that there is sufficient space left on .the tyre record originally made out when the cover was supplied new, a heavy horizontal line could denote the demarcation when retreading took place. In some instances, however, it might be more convenient to issue a new tyre record form, when the remould was received back into stock, and add the letters RM before the serial number of the cover to denote the change.

Discarded Cover It should be borne in mind, however, that when completing the cost section of the tyre records, allowance should be made for any sum received for the discarded cover. Similarly, if a new form is made out when a remould is received back into stock, an equal amount, together with the cost of remoulding, should be debited against that cover in the same way as the initial price is debited against the new. tyre.

Theoretically, the tyre cost records should include not only the cost of the cover but also tubes and flaps, but this is impracticable because changes of cover, tubes and flaps do not always coincide. As tubes and flaps represent only a small proportion of the total tyre cost, averaging out the expenditure on them over the whole fleet and then dividing it in proportion to the number of wheels per vehicle will be sufficiently accurate. Even so, a check should be made from time to time to ensure that the total number of tubes and flaps used throughout the period corresponds to the number of covers fitted.

A recommended Tyre Change Form is shown in Fig. 2. Once the tyre record system has been put into operation, this is the form which will be used most regularly. It is drawn up as simply as possible, bearing in mind that it will probably be filled in by the fitter, or tyre fitter if the company is large enough to employ a member of the staff especially for that purpose, For the same reason it should not be too small or flimsy.

This form is divided into four sections. In the first is recorded the vehicle number, wheel position, date and mileometer reading. The serial letters and number, size, ply and make of tyre removed are then entered, followed by corresponding details of the tyre fitted. The fitter's remarks and signature complete the form. When a new vehicle is received it should not be overlooked that tyre record forms must be made out for each tyre fitted as original equipment, in addition to new or remoulded tyres received direct into stock.

Left and Right In completing both of these forms, a need will be found for convenient abbreviations of tyre position. Traditionally, in this country at least, the terms "neat side" and "off side" have been commonly used, but partly as a result of increasing export trade there has been a growing tendency to state simply "left," or "right." The distinction between twin tyres when fitted is shown by (1)—inner—or (0)—outer. With the increasing use of multi-axled vehicles the simplest method of denoting relative positions is to number the axles from front to rear.

By the' combination of these abbreviations any tyre on an eight-wheeler can be clearly indicated by a maximum of three letters or numbers. Thus, 2112 would indicate the kecond steering axle right (or off) side, whilst 4/140 would denote the outer cover on the left (or near) side of the second rear axle.

Abbreviations for the six wheel positions on a four-wheeler with twin rear tyres would thus read: Front, 1/1,--1/R; rear, 2/L/0-2/R/0; 2/L/I-2/R/I.

Similarly for a four-wheel-steering six-wheeler the abbreviations would read: Front, 1/L—I/R; 2nd front, 2/L-2/R; rear, -3/L/0-3/R/0; 3/L/I-3/R/I.

The criticism could be made that when using this system. " 2 " could indicate three different axle positions—the rear axle of a four-wheeler, the second front axle of either a four-wheelsteering six-wheeler or eight-wheeler, and, in addition, the first of the two rear axles of conventional rear-bogie sixwheelers. Whilst this is correct, it should prove no handicap where the user is sufficiently familiar with his vehicles to recognize the type from the vehicle number.

Alternatively, with larger operators, this information would be available from the fleet number if the method of vehicle designation recommended previously in these articles has been adopted. Having then allocated blocks of fleet numbers to each type of vehicle (as opposed to chronologically), the precise wheel positions would be shown on the tyre record form by a combination of fleet number and tyre position abbreviation recommended here.

The filing of tyre record forms allows for some variation relative to each user's size and type of fleet and operational conditions. In addition to a simple filing according to make, serial letter and number, grouping into sizes would facilitate segregation of costs. • S.B.