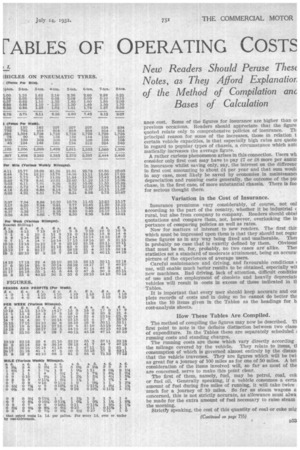

"THE COMMERCIAL MOTOR" FABLES OF OPERATING COSTS

Page 50

Page 51

Page 55

Page 59

If you've noticed an error in this article please click here to report it so we can fix it.

11 VERY new edition of these Tables involves two points in the _LA way of introduction: (a) an explanation of the bases of the Tables and their method of compilation, so that new readers may understand, and (b) notes regarding alterations which are of Interest to established readers.

It is logical and reasonable first to consider old readers, so that they need not read through the whole of this introduction in order to come to that part of it which concerns them. New readers will find all of this matter of very considerable interest.

So far as old readers are concerned, the most salient point of difference to be noted is the splitting up of the standing charges and the tables of total cost into 48-hour and 96-hour weeks. This is really little more than an acknowledgment of the fact that in the operation of bus services and some coach services, double shifts are necessary. Then, 'having admitted the need for that acknowledgment in one direction it seemed advisable to extend it throughout the Tables. The only exception made is in respect of electric-battery vehicles, which, for obvious reasons, are not susceptible to such use.

Pneumatic-tyred Steam Wagons Now Included.

The addition of a new table for pneumatic-tyred steamers was to be expected. Readers should appreciate that this has been made possible only after considerable research and investigation into the experiences of users.

Less obvious, but perhaps, more important, are the detail alterations in cost. The trend up to the time of writing is still in a downward direction. The cost of operation of nearly every class of commercial vehicle is somewhat less than as shown in the previous edition of these Tables. Petrol, notwithstanding a further addition to the already heavy taxation, is still 3d. per gallon cheaper than it was before. In the Tables the figure of is. 1c1,... per gallon is taken instead of is. 4d.

The cost of tyres is less for two reasons. The list price is lower and tyres are giving even better service than previously. Tile latest and best tyres can be expected to afford 15 per cent. to 20 per cent, longer life, whilst the prices are actually from 10 per cent. to 15 per cent. lower than they were when the previous edition of these Tables was compiled. In modifying figures for tyre costs we have not gone all the way in acknowledging these advantages, but have allowed only about 50 per cent, of the improvement which is ultimately possible. That is strictly in accordance with the established custom of quoting average results and not extreme figures.

One point in particular arises from this feature and that is the importance of buying only the best tyres if the lowest figure for operating cost is to be attained. This has always been a sound policy, but it is now more necessary than ever.

Provision for Interest on First Cost.

The importance of the item of interest on first cost, always disputed, is emphasized when comparing this year's Tables with previous issues, for they afford, in the diminished figures for interest, an example of how that item operates. It is customary to calculate the figure at 1 per cent, above bank rate, which means that this year it need be taken at only 8i per cent. instead of 5 per cent. The reader will better appreciate this if he regard it from the point of view that the lower the figure of interest on first cost the more easily should he be able to obtain money to invest in new rolling stock.

Against these economies must be set a slight increase in insur)332 once cost. Some of the figures for insurance are higher than m previous occaalons. Readers should appreciate that the figure quoted relate only to comprehensive policies of insurance. Th principal reason for some of the increases, those in relation t certain vehicle capacities, is that especially high rates are quote in regard to popular types of chassis, a circumstance which auk matically increases the average figure.

A rather curious phenomenon arises in this connection. Users wh consider only first cost may have to pay ET or ES more per annur in insurance whilst saving only, say, the interest on the differenc

in first cost amounting to about per year and that sum woult in any case, most likely be saved by economies in maintenanc( depreciation and running costs generally, the outcome of the pui chase, in the first case, of more substantial chassis. There is foo for serious thought there.

Variation in the Cost of Insurance.

Insurance premiums vary considerably, of course, not onl according to the part of the country, whether it be Industrial c rural, but also from company to company. Readers should obtai quotations and compare them, not, however, overlooking the in portance of comparing policies as well as rates.

Now for matters of interest to new readers. The first thin which must be impressed upon them is that they should not regar these figures as in any way being fixed and unalterable. Ther is probably no case that is exactly defined by them. Obvious] that must be so, for, probably, no two cases are' alike. The statistics set a standard of moderate attainment, being an accurai picture of the experiences of average users.

Careful maintenance and driving, and favourable conditions use, will enable much better results to be obtained, especially wil new machines. Bad driving, lack of attention, difficult conditica of use and the employment of obsolete and heavily depreciatE vehicles will result in costs in excess of those indicated in ti Tables.

It is important that every user should keep accurate and cor plete records of costs and in doing so he cannot do better tho take the 10 items given in the Tables as the headings for h cost-analysis sheets.

How These Tables Are Compiled.

The method of compiling the figures may now be described. TI first point to note is the definite distinction between two class! of expenditure. In the Tables these are separately scheduled running costs and standing charges.

The running costs are those which vary directly according the mileage covered by the vehicle. They relate to items, ti consumption of which is governed almost entirely by the distan, that the vehicle traverses. They are figures which will be twi, as great for a journey of 100 miles as for one of 50 miles. A bri consideration of the items involved will, so far as most of the are concerned, serve to make this point clear.

The first of them, namely, fuel, may be petrol, coal, cok or fuel oil. Generally speaking, if a vehicle consumes a certa amount of fuel during five miles of running, it will take twice much for a journey of 10 miles. So far as steam wagons a concerned, this is not strictly accurate, as allowance must alwa. be made for the extra amount of fuel necessary to raise steam the morning.

Strictly speaking, the cost of this quantity of coal or coke mig

almost be set down as a standing charge. It is, however, unfortunately too indeterminate for that and has to be approximated to in the figures for coal consumption. This course is rendered the easier by the fact that averages form the basis of the figures given, and in those means the allowance for fuel for steam raising automatically enters.

The figures for petrol are calculated on the basis of Is. Id. per gallon, and for coal at £2 5s, per ton. The reader who is paying more or less than these amounts can correct his figures according to the footnote to each table. So far as electric vehicles are concerned, their "fuel" is the current which they take from the mains. It is assumed that the cost of that current is 1.d. per unit. Oil is assumed to cost 3s. per gallon.

The life of pneumatic tyres varies according to size, and there is, indeed, a point in the upward scale of sizes at which a considerable difference prevails between the expectation of life of one size and that of the next above it. So far as the figures for cost of pneumatic tyres are concerned, it is, therefore, impossible to state in this introduction the actual mileage on which the figures are calculated, because that mileage differs. Averages are taken and the costs are corrected according to current list prices, less a discount which is, nowadays, generally awarded to commercialvehicle users.

Maintenance is an " omnibus" term that really relates to every item of expenditure, not justifiably included in the sections devoted to fuel, oil or tyres, involved in connection -with the running of a commercial vehicle. It refers, therefore, not merely and solely to the cost of repairs, as is wrongly assumed by many readers and users of the Tables, but to such expenditure as washing and polishing, the purchase of sundry supplies, the cost of decarbonizing, greasing, changing the oil in the engine case, replacing lamp bulbs, and a host of other things that are small in themselves, but, in the aggregate, amount in the course of a year to quite a considerable sum. Frequent references to this item and indications of means whereby it can be properly assessed appear from time to time in the series of articles entitled " Problems of the Haulier and Carrier," which are a regular feature of The Commercial Motor.

Depreciation is calculated on the assumption-which, incidentally, average figures have shown to be reasonablethat the life of a vehicle extends to 150,000 miles of running. It is sometimes held that depreciation is a standing charge. That is wrong, but it has to be admitted that there is this difficulty: income tax assessors ask for it to be recorded as such, on the basis of an annual depreciation of 20 per cent. per annum, on the book value of the vehicle. That, however, is not the correct way to calculate depreciation for purposes of ascertaining the operating cost of the vehicle itself, as will be appreciated when it is realized that whilst many ordinary commercial-vehicle operators regard 10,000 miles to 12,000 miles as reasonable use of a heavy lorry, haulage contractors customarily expect, three, four or five times that distance in a year. Of late, motor-coach owners have been reaching six-figure mileages in the course of a year. To calculate the depreciation of the latter type of vehicle on the basis of 20 per cent, per annum is impracticable.

The standing charges are more easily described and understood. To a large extent—in fact, with one exception— they are almost arbitrary. The exception is the first. on the list, namely, the annual amount which has to be paid for taxation. All the standing charges have this in common, they do not vary with the mileage of the vehicle, but, in the ordinary course of events, remain unaffected thereby.

Wages in these Tables are set down in accordance with trades-union rates, wherever those apply. It is the duty of users whose figures differ from these to make corrections accordingly. They are not bound, in any way, to these figures, but need take them as only an approximate guide. The same applies to .the next two items, namely, rent and rates and insurance.

Only the last one—interest on first cost—calls for.discussion. Some men refuse to entertain the idea that this item should be included at all, whilst others agree not only that it should be included but that the figures which appear in the Tables are correct.

In between those two extremes there is another opinion, that the item should have the value depreciating with that of the vehicle.. Actually, if the item of depreciation was treated as it should be, and if the amount of depreciation was set aside towards the purchase of a new vehicle, the interest on that sinking fund would have the -effect of counteracting the incidence of interest on first cost, so as gradually to reduce it as time passed.

In those circumstances, a rough approximation wiyuld be to halve the figure for interest given in the Tables and let that stand as the average throughout the life of the vehicle. Where, however, there is no sinking fund established there is no justification for regarding the itein of interest as being in any way less than that included in the Tables. Both interest and depreciation are calculated on the net cost of the complete vehicle, less the cost of a set of tyres. This correction is necessary because tyres appear as a separate item.

It remains now to refer only to the fact of each table appearing below the heading "Hauliers' Figures." These Tables are widely used by haulage contractors as a basis for the calculation of the charges which they should make to their customers, and to help them to that end certain arbitrary figures for establishment charges and profit are assumed. These are added to the total cost for various mileages and an appropriate charge is arrived at accordingly.

Here, again, the reader whose views as to the amount of his establishment charges and as to what constitutes reasonable profit differ from ours must accordingly correct the figures, but he must never make the mistake of assuming that he has no establishment charges.