Cover All Your Costs When Hiring Out Cars

Page 70

Page 73

If you've noticed an error in this article please click here to report it so we can fix it.

THE problems in the business of private hire of cars are difficult: not least of the troubles which beset operators crop up when the choice of vehicle is made. Sometimes large cars are selected and it is in connection with these that most of the complexities arise where rates and fares are concerned. I have not dealt with this subject for some time, so perhaps some information about this department of the industry would be of value.

Perhaps the first thing to do is to differentiate between private and public hire. The vehicles employed on public hire have to be licensed accordingly. Generally a vehicle must carry a plate to indicate that it is so licensed. A taxicab owner is practically a public servant. His licence permits him to ply for hire on the public streets and, in return for that privilege he must accept any responsible person as a fare.

The private-hire car does not use the highways as stands and must not do so. It must be hired at the garage where it is customarily housed or at some office. There is no need to obtain any specific licence for the usc of a car on private hire. Duty must, be paid on each car under the schedule "Motor HacknO Vehicles." For vehicles with a seating capacity not exceeding four passengers, the duty is £10 per annum, and with a seating capacity exceeding four passengers but not exceeding eight the tax is scaled at £12 per annum.

Hackney Carriage

A hackney carriage is defined as a mechanically propelled vehicle standing or plying for hire and includes a mechanically propelled vehicle let for hire by a person whose trade it is to sell such vehicles or let them for hire, provided that the vehicle is not let for a period amounting to three months or more.

If, as the result of taxing a vehicle at the hackney carriage rate of duty, the tax paid is less than would have been payable at the private-car rate, the vehicle must carry the prescribed hackney carriage plate above the rear identification mark. If the private-car rate of duty is paid when it is the higher of the two, the plate need not be displayed, even if the vehicle is used as a hackney carriage; nor is it necessary if the vehicle is licensed to ply for hire and carries c30 a distinguishing mark to that effect, as it becomes superfluous in that case.

The biggest concerns that arc engaged in the private-hire business in large cities prefer high-powered cars of 30 h.p. or 40 h.p. according to the old R.A.C. rating. The reason appears to be that in the provinces, at any rate, an imposing appearance is regarded as outweighing the payment of a high tax. The companies obviously have found that the class of customer who makes use of their cars is so appreciative of them as to be willing to pay the rates which the enjoyment of such expensive machines compel their owners to charge.

This partiality for large arid imposing-looking vehicles is not confined to big undertakings. Many car hirers in a small way of business have the same preference, but not having, as a rule, sufficient capital to enable them to buy new vehicles of this description, they usually purchase them used.

Pass Through Many Hands

The fact that the big companies are in the habit of depreciating their vehicles heavily and selling them at the end of the third or fourth year of use is fortunate for those who are compelled to look to the used market for their vehicles as the mainstays of their businesses. There is no doubt that cars of this type pass through many hands before the days of their use as hire cars are ended, for they are seen in all stages of age and serviceability, although their condition is generally fairly high.

.There are, however, certain disabilities attached to the use of such big cars, apart from the high initial cost, notably the expense of operation, and there has been a tendency of late, particularly among provincial hirers, to depart from this preference for big cars and to use vehicles or less power and weight. The hiring concerns have been encouraged in that by manufacturers of both touring cars and taxicabs, who are now offering vehicles particularly adaptable for hire work and usually known in the industry as provincialtype taxicabs.

They are more roomy, more luxurious and generally more adaptable to this service than the London taxicab, which to he built to comply with certain limitations imposed zabs plying for hire in the district covered by Metro:an police regulations.

some cases, enterprising car hirers of an economical ie of mind have gone further and selected 10 h.p. chassis the purpose. Only occasionally is this extreme measure fled; as a rule the experiment terminates soon in the iange of that vehicle for another with a little more rve of power. This is, after all, only what might have I expected. A hire car, to be satisfactory, must have iirly heavy body, besides being called upon, as often ot, to carry its full complement of passengers as weJ1 as age.

onsideration of the economics of a private-hire business of course, into Iwo divisions, namely expenditure and me. The first resolves itself into three main sections. re is the cost of operation of the business, the cost of ntaining the cars, and the actual cost of running them. o limit the scope of this article, I am going to restrict elf to the consideration of businesses in which there several vehicles: for convenience 1 will take as an npie a minimum of three. For the time tieing, the ler-driver with one vehicle only is best left out of the ition.

Establishment Costs

aking first of all the cost of operating the business, tier readers of these articles, which are mainly coned with haulage of goods, will recognize that I am at to deal with what, as a rule, I refer to as establishment s or overheads. An office will be necessary and a telene is essential. The staff may comprise a clerk who is : to type out accounts, take telephone messages and, a schedule of engagements available, accept orders, re will be expenditure on postage, telegrams and other ie sundries. Finally, there, is to be provision for the ry of the owner himself, who will, as it were, rank as irector of the firm.

,ssume that the office rent per week is £1. The telephone cost about the same amount. The clerk will expect Ler more than £6 lOs per week. Allow for sundries at per week. The managing director will draw, as his ry, about £10 per week. These are the main items only they amount to £19. A figure of £21 will serve.

should be noted that there is no provision made for a tirs department. Actually provision is made for the of repairs in the item "maintenance" in the schedule unning costs of the vehicles. Allowance is not made for wages of a second driver. In cases where experience shown that an extra driver should be engaged a correcmust be made accordingly.

Expert Help for Accounts

he foregoing are representative of the average of estabment costs of a concern operating three vehicles. If e are more than three, the establishment expenses will ease, because extra expert help will be needed to sort out :rs and to keep track of accounts, and it may be taken roughly a further £5 will be needed per week per ear, come now to the actual operating costs of the vehicles.

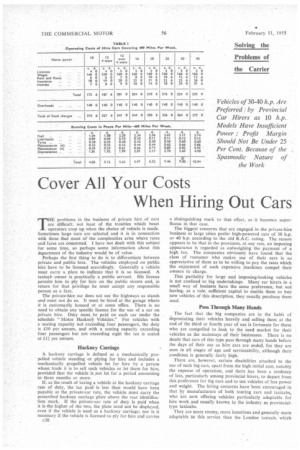

t there are the standing charges, that is to say, the enditure which is fairly regular week by week, not in way governed or even affected by the mileage run, items are well known and are, in any event, included the accompanying Table, which is extracted from 4e 13 of " 'The Commercial Motor Tables of Operating ts."

he standing charges vary somewhat according to the and type of the vehicle; similar diversion is to be noted :he running costs to perhaps a greater extent, This le, like those in the Tables, gives average figures both running costs and for standing charges and will serve guide so long as readers do not take them too literally. many cases the figures can be improved upon but in svourable conditions the opposite will apply.

this Table, figures for a 10 h.p. car are given in ignition of the fact that certain operators favour this In my, view such vehicles are under-powered for or hire-car work, but that is really by the way.

On examining the Table the reader will observe that there are three items for each class of car: there is the establishment charge of £7 per week; the Standing charges, which vary from £8 15s. per week to £11 15s., and the running costs which run from 4.82d. per mile for the 10 h.p. car to 10.94d. per mile for the 40 h.p. machine.

• Impulsive readers may take the wrong view of the 10.94d. for the running costs of the large car, urging that it is insufficient. They must hotel their horses for a bit: the figure for running costs is not all by a long way. .

Running Expenses

The careful reader will appreciate that whilst he can sum the overhead and standing charges to arrive at a total per week for each type of car, he cannot deal so easily with the running costs, for they must be translated into a cost per week to make the addition practicable. Before that can be done some idea of the weekly mileage which the vehicle is likely to cover must be known. Then. by multiplying the number of miles by the running cost per mile the cost per week can be obtained.

Alternatively, the total of establishment costs and standing charges, or those items taken separately, may be divided by the weekly mileage and the result added to the running cost per mile. This will give a total operating cost per mile, including overheads.

Following the latter procedure and taking as an example a 12-h.p. car licensed to carry more than four passengers, divide first the establishment charges—£7—by 400 (4.20) and then the standing charges, £10 Is, per week, by 400 (6.03d.); by adding the running costs per mile (5.63d.) we arrive at 15.86d. as the total cost per mile of running each car of this fleet.

The total cost per week is easily obtained by multiplying that figure by 400, which represents the mileage. It amounts to £26 8s. 8d., which, on the basis of a 44-hour week, is equal to a fraction over 12s. per hour.

I have not as yet considered the profit. On work of this nature, which is spasmodic rather than regular, the profit margin should not be less than 25%. On that basis the total earnings should be not less than £33 Os. 8d. That means that the minimum charge per mile must be Is. 8d.

2s. A Mile Rate

It remains to apply these rates to the various kinds of hire business scheduled by a hire-car owner. For country yuns Is. 8d. is the minimum charge per mile. (Get 2s. if it can be obtained.) On point-to-point runs on which the mileage is reckoned only one way, the minimum charge must be 3s. 4d. per mile. Even at that there must be a certain loss of profit, because of the dead mileage from the owner's garage to the point at which it is proposed to pick up the passenger or passengers.

For shopping, visiting, sightseeing and similar town work, time should be charged at 16s. per hour plus the mileage run at Is. Bd. per mile. Theatre trips, with a maximum of four hours and 25 miles, may be done at 64s. for the time (four times 16s.) plus 9d. per mile run. A dinner and theatre journey including six hours should be charged at £5, which is six times 16s. per hour plus a small allowance for the mileage.

One more point, for new readers who have not followed Closely the articles on operating costs which are a regular feature of The Commercial Motor—the item "interest on first cost" is included because without it the schedule of standing charges would not be complete. It is not an expenditure but a revenue. The amount set down is the interest on the money laid out on the car and actually returns to the pocket of the owner if the foregoing amounts are received as fares and charges. S.T.R.