BUYING TIME

Page 48

Page 49

Page 50

If you've noticed an error in this article please click here to report it so we can fix it.

Financial and accounting jargon is almost as bewildering as computer jargon, so we have tried to provide a simple guide through the jungle, and to show which method of vehicle acquisition is the most cost-effective.

LTo buy or not to buy: that is the question. Most large transport fleets are now operated on what used to be called the "never never". No-one actually seems to buy them: the industry is full of operational leasing agreements, vast contract hire deals and buy-back clauses.

Operators face a financial jungle full of competing money men, all claiming that their system is the best. For most big operators, owning trucks is considered crazy at best, suicidal at worst, because they depreciate and do terrible things to the health of your balance sheets. Contract hire and SSAP21, the Statement of Standard Accounting Practice, allows companies to get their trucks off the balance sheet and improve both their gearings and their loan qualifications.

The factors which should influence your vehicle replacement policy are: 0 The original capital cost as well as the suitability of different vehicle types; 0 The expenditure involved in operating and maintaining the vehicle (if responsibility falls on the user); 0 The effect on income of the use of such a vehicle; 0 The method of financing the acquisition (for example by borrowing); 0 The impact of taxation on the vehicle acquisition.

There are three main methods of funding and evaluating your vehicle fleet once you have taken those factors into account.

Rate of Return expresses the average rate of return as a percentage of capital invested. It represents the natural approach to the problem because under it the project showing the highest profit over the life of the asset is selected. Its disadvantage is that although it may select the project which shows the greatest rate of return, it fails to take into account the actual incidence of expenditure and income although this incidence does have a significant financial effect.

Payback refers to the period over which the original capital and other costs are "recovered" (met out of the cash income). It takes account of the timing of the related income and expenditure. The objection to it is that since it selects the shortest period for "recovery" of costs, it does not take into account the total of these recoveries over the whole life of the vehicle.

Discounted Cash Flow (DCF) recognises that the application of money (or finance) itself has a cost and that that in itself is an important element in the assessment. What matters is that any decision taken involves a cash outlay, either immediately or over a short period of time associated with some continuing cash expenditure that may be compensated for by a cash inflow in the future. It is necessary to judge whether future cash earnings will adequately compensate for the initial and subsequent cash outlay and in addition provide an acceptable return. Obviously cash expenditure, whether on buying a new asset outright or on some method of hiring one, represents a sacrifice since it could be directed towards producing a cash income (for example by investing it through making a bank deposit or acquiring some interest in another undertaking, or even by paying off a loan, thus reducing the current level of cash outgoings). Corresponding cash income can itself be used to produce further income by way of interest.

This must be fundamental to any evaluation of a project involving finance and it underlies the DCF appraisal technique.

DCF takes account of all cash flows on the basis that a sum of money forgone or received at a particular time differs in value to the recipient if the payment is delayed or advanced. In other words, DCF takes into account the interest factor which must be compounded for the purpose of comparison.

The drawbacks are that payback and DCF methods are based on cash transactions and not on ordinary income and expenditure transactions (they exclude depreciation, for example). Moreover, they take into account the cash impact of taxation normally delayed somewhat, the liability being settled only some time after the accounting period to which it relates. The rate of return approach does not normally take into account the tax implications — at least not normally in specific terms, but the main drawback with the rate of return system is that it deals with depreciation as an item of expense — which is correct from the point of view of the ordinary method of calculating the rate of return. Depreciation, however, while recognised as an element of expenditure for normal purposes, does not represent a cash item.

No cash is expended through charging depreciation, though the depreciation charges in fact represent the recovery of cash. In one way or another, there is an interest benefit.

When you do not want to make an outright purchase, possibly because of a cash shortage, various other methods of finance are possible. Legally they all differ slightly, but to make the right decision, they must all be evaluated by the same techniques.

BORROWING TO BUY

A degree of borrowing is an essential part

of nearly every company's activities. Any return generated which exceeds the cost of funds adds to return on equity and shareholders' funds, but the level of borrowing needs to be controlled unless it becomes too high a fixed cost which has to be overcome before profit can be earned. It is therefore important to be able to match the repayment of borrowing with the use of the asset. The ease with which borrowed funds can be repaid can be of critical importance.

It is for this reason that asset-based finance is so attractive. The ability to repay loans by sale of specific assets is useful, although that ability can only be retained if the loan is paid down as the asset's value falls.

Vehicle fleets may be regarded as assets which are less fundamental to the operation of the business and may be more easily realised than buildings, stock, work in progress or debts. They can therefore be viewed as attractive assets against which to raise finance. The borrowing just discussed could just as easily take the form of HP or a lease. Though the most obvious, loan finance is only one way of borrowing.

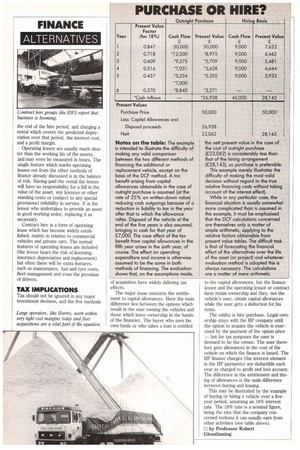

HIRE PURCHASE

As a traditional player in the consumer market, hire purchase is often over-looked as a source of finance for business. In essence it is little different from a finance lease with a bargain purchase option built in. If the deals are big enough interest rates for HP transactions need be no different than loan rates. On smaller deals, however, implicit interest rates can be very high. HP offers an automatic method of retiring loans over the life of the asset in question.

FINANCE LEASES

Under a finance lease the vehicle is never owned by the lessee, who simply pays a rental for its use. The rental pays the lessor's capital cost plus interest plus profit over the primary period of the lease. Just as with loans and HP, however, all the real costs of ownership such as maintenance and insurance are retained by the lessee.

Though the lessor may make an estimate of residual value in arriving at the timing of rentals, the risk remains with the lessee. When the assets in question are sold the lessor will require a final rental equal to the discounted value of any unpaid rentals. When the sales proceeds are to hand the lessor will give a rental rebate to the lessee, usually 95 to 99%, so the lessee must fund the full cost of the asset and bear the risk of a lower residual value.

OPERATING LEASE AND CONTRACT HIRE

Operating leases are based on the lessor or contract hire company acquiring the vehicles, predicting their residual value at • the end of the hire period, and charging a rental which covers the predicted depreciation over that period, the interest cost, and a profit margin.

Operating leases are usually much shorter than the working life of the assets, and may even be measured in hours. The single feature which marks operating leases out from the other methods of finance already discussed is in the balance of risk. Having paid the rental the lessee will have no responsibility for a fall in the value of the asset, any licences or other standing costs or (subject to any special provisions) reliability in service. It is the lessor who undertakes to provide an asset in good working order, replacing it as necessary.

Contract hire is a form of operating lease which has become widely established, mainly in relation to commercial vehicles and private cars. The normal features of operating leases are included (the lessor bears the risk of licensing, insurance depreciation and replacement) but often there will be extra features, such as maintenance, fuel and tyre costs, fleet management and even the provision of drivers.

TAX IMPLICATIONS

Tax should not be ignored in any major investment decision, and the five methods of acquisition have widely differing tax effects.

The major issue concerns the entitlement to capital allowances. Here the main difference lies between the options which result in the user owning the vehicles and those which leave ownership in the hands of the financier. The buyer who uses his own funds or who takes a loan is entitled to the capital allowances, but the finance lessor and the operating lessor or contract hirer retain ownership and they, not the vehicle's user, obtain capital allowances while the user gets a deduction for his rents.

The oddity is hire purchase. Legal ownership stays with the HP company until the option to acquire the vehicle is exercised by the payment of the option price — but for tax purposes the user is deemed to be the owner. The user therefore gets allowances in the cost of the vehicle on which the finance is based. The HP finance charges (the interest element in the HP payments) are deductible each year as charged to profit and loss account. The difference in the entitlement and timing of allowances is the main difference between buying and leasing.

This may be illustrated by the example of buying or hiring a vehicle over a fiveyear period, assuming an 18% interest rate. The 18% rate is a nominal figure, being the rate that the company concerned reckons it can usually earn from other activities (see table above). 0 by Professor Robert Glenditming