PROBLEMS 01 the HAULIER and CARRIER

Page 60

Page 61

If you've noticed an error in this article please click here to report it so we can fix it.

More Details of the Simplified System of Cost-keeping which " S.T.R. " is Recommending to His Many Readers as a New Year's Procedure

BEFORE proceeding any farther with the description of my system of book-keeping, I should like to make myself clear on one or two points. First of all, there is nothing in the system that I am about to describe which calls for expert assistance. It is devised so that those persons who are least familiar with figures can make use of it. It is not suggested that it should be preferred to any existing system, or substituted therefor. Those readers whp are already keeping records of costs should stick to them, provided they be satisfied that they are complete and accurate.

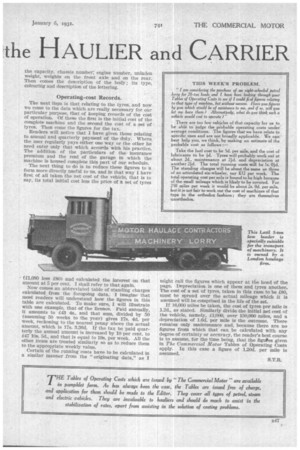

The system I have in view is designed to help the Table I.—Fly-leaf of Operating Costs Record Book.

Vehicle No.: 1. Rigistered No.: CM1931.

Make and Model: Nubian Sparrow. Capacity: 4 tons net.

Chassis No.: VX 1235784. Engine No.: VX 785342,

Unladen Weight: 3 tons IS cwt.

Front Axle: 4 tons. Rear Axle: 8 tons. Body: Platform with high, binged sides.

Colour: Green with yellow lettering. . Tyres: Pneumatic, 36 in. by 8 in., twins on rear wheels.

Initial Cost: £1,080. Cost of Tyres: £80. Tax: £43 4s. Od. per annum. (147 10s. 5d., if paid quarterly.) Insurance Premium: £27 10s. per annum.

Garage Rent: £27 10s. per annum. man with no experience, and its principal objective is the prevention of oversight ; it will,obviate the risk of any item of expense being overlooked. That, as I explained in the previous article, is where so many hauliers go wrong; even amongst those who do keep costs of some kind or other—more or less accurate costs, after systems of their own—and an examination of this system will disclose the fact that it is based on The Commercial Motor' Tables of Operating Costs, so that it can be used and worked in conjunction with those Tables and thus facilitate the process of comparison between estimated and actual costs which is recommended as one of the functions of the Tables.

The second principal object that I have kept in mind in preparing the system is the need which the haulier has for kiaowiug his costs from day to day, and from the time that he first begins to operate his vehicle as a means for earning a living.

Now the main difficulty in the way of obtaining that essential information from the start, apart from making direct use of our Tables, which, up to date, provide, I may say, the only method.of estimating operating costs on a rational basis, is that the newcomer has no definite information as to cost of tyres, or of maintenance: he is apt, too, to overlook the item of depreciation. It will be neted, and I shall indicate, that adequate provision is made against any of these eventualities.

Explaining the Specimen Fly-leaf.

Referring now to the specimen fly-leaf of the book in which the actual operating costs are to be recorded, the reader who recalls what I wrote in the previous article will note that there is more on it than he has been led to imagine. There is no more than I had in mind at the time I wrote that article, for what is there is merely amplification of what I suggested should be the basis of the records on that page. I will explain.

The first thing to do is to realize that each vehicle must have its own separate book : there must be no attempt made to economize by trying to make oncebook serve for several machines, for that is the way to complication and inaccurate records and that, more than anything, is what we are endeavouring to avoid.

An accurate and complete description of the vehicle comes first. At the top is its consecutive number, that by whic_h it is known. in the office, as it we-re. I have taken No. 1 to serve lny purpose there. Then comes the registered number. That is what might be termed an identification mark.

The description of the vehicle comes next, and it will be observed that all the particulars needed for registration purposes are entered there. There is the make,

the capacity, chassis number; engine number, unladen weight, weights on the front axle and on the rear. Then comes the description of the body; its type, colouring and description of the lettering.

Operating-cost Records.

The next ite,m is that relating to the tyres, and now we come to the data which are really necessary for our particular purpose, that of keeping records of the cost of operation. Of these the first is the initial cost of the complete machine and the second the cost of a set of tyres. Then come the figures for the tax.

'leaders will notice that I have given those relating_ to annual and quarterly payment of the duty. Where, the user regularly pays either one way or the other he need enter only that which accords with his practice. The addition of the particulars of the insurance premium and the rent of the garage in which the machine is housed complete this part of our schedule.

The next thing to do is to reduce these figures to 'a form more directly useful to us, and -in that way I have first of all taken the net cost of the vehicle, that is to say, its total initial cost less the price of a set of tyres

(£1,080 less LSO) and calculated the interest on that amount at 5 per cent. I shall refer to that again. Now comes.an abbreviated table of standing charges calculated from the foregoing data. I imagine that most readers will understand how the figures in this table are calculated. To make sure, I will illustrate with one example, that of the licence. Paid annually, it amounts to £43 4s., and that sum, divided by 50 (assuming 50 weeks to the Tear) gives 17s. 4d, per week, reckoning to the nearest penny 'above the actual amount, which is 17s. 3.36d. If the tax be paid quarterly the annual amount is increased hy 10 per cent. to £47 10s. lid., and that is equal to 19s. per week. All the other items are treated similarly so a to reduce them to the appropriate weekly value.

Certain of the running costs have to be calculated in a similar manner from the "originating data," as I

might call the figures which appear at die head of the page. Depreciation is one of them and tyres another. The cost -of a set of tyres, taken in this case to be £80, must be spread over the actual mileage which it is assumed will be comprised in the life of the set.

If 16,000 miles be taken, the cost of -tyres per mile is 1.2d., as stated. Similarly divide the initial net cost of the vehicle, namely, £1;000, over 150,000 miles, and a depreciation of 1.6d. per mile is the outcome. There remains only maintenance and, because there are no figures from which that can be calculated with any degree of certainty or accuracy, the reader's best course is to assume, for the time being, that the figutes given in The Commercial Motor Tables of Operating Costs apply. In this case a figure of 1.20d. per mile is assumed, S.T.R.