BEATING THE VAT TRAP

Page 38

Page 39

If you've noticed an error in this article please click here to report it so we can fix it.

There is no escape: no matter where you go the taxman follows. The best way to • keep him happy is to get your accounts well organised. We have a few helpful hints to bring you a quieter life.

• It is said that the only two certainties in this life are death and taxation. You could add a third certainty — more taxation in the form of penalties for the late payment of taxes.

In the past, many road hauage companies have regarded Her Majesty's Government as a prime source of finance by withholding tax payments until the last possible moment. During the 60s and 70s this was almost a national business sport as the tax authorities took a very benign and relaxed approach to collecting back taxes.

The last decade has seen the Government toughen up these attitudes_ Now it seems as if the Government has devised methods for the collection of taxes which operate rather like that medieval instrument of torture, the rack.

Taxmen these days come in two guises. Both are after your money. There is the Vatman employed by HM Commissioners of Customs and Excise, and the Collector of Taxes employed by

the Inland Revenue.

It is the Vatrnan who has changed his spots the most. Customs and Excise used to be very tolerant of late payment of VAT, particularly if you waited for the estimated assessment to arrive a month or so after the due date. Often it would also be on the low side and there would be no need to pay until a few weeks later. They would sometimes get tough, though not very often, even though tax related penalties were actually around in 1980 for the late payment of VAT.

The atmosphere changed for the worst with the introduction of the Finance Act 1985 which introduced a broad range of nasty weapons. A further programme of changes has taken place since and these will continue until at least the middle of 1988. Almost each month sees the introduction of some new regulation or other and many road hauliers, busy running their businesses, have been caught out.

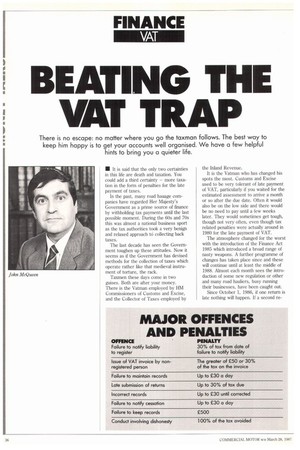

Since October 1, 1986, if one return is Late nothing will happen. If a second re turn is late within the next year a formal warning in the form of a "surcharge Liability notice" will be issued. This is the first of a progressive series of turns of the screw. If a third return is late within the next 12 months then the haulier (known by the Customs and Excise as a trader) will be charged a surcharge of 5% on the VAT bill payable on that return.

For each subsequent late return (unless the taxpayer returns to good behaviour for a year) the surcharge increases to 10%, 15%, 20%, 25% and finally a staggering 30%. The Government presumably believes that this level of pain will be sufficient to bring any recalcitrant taxpayer to his knees.

Already a number of hauliers with cash flow problems have been caught by the new changes. It is often those hauliers who can least afford to be caught by the new penalties who are feeling the brunt of them.

VAT regulations say that these surcharges will only apply to: "traders who are persistently late in sending in their returns or paying VAT due", though it seems questionable if being a few days late three times out of ten can be described as persistent. For practical purposes even being one day late can be defined as "late". Customs and Excise will even go to the trouble of recording the date of the postmark in deciding whether a return was despatched at a reasonable time for it to reach Customs on the due date.

FRAUDULENT EVASION

On top of this, you should realise that the fraudulent evasion of VAT, the issue of documents to deceive and the deliberate issue of false statements are criminal offences. Many businessmen have gone to prison for these offences.

Plans for the future include interest to be charged on overdue VAT (and overdue penalties) as well as daily penalties for breaches of certain regulations yet to be announced. Appeals are possible against these penalties but the onus of proof will be on the taxpayer. If a taxpayer dies then this would be accepted as a reasonable excuse for neglecting vAT returns!

These penalties are daunting, particularly for small businesses already overburdened with paperwork. Consequently, the Government is now seeking an EEC agreement to allow businesses with an annual turnover below £250,000 to account for VAT on the basis of cash received and paid out. Traders will not have to account for VAT until paid by their customers and will not be able to reclaim VAT until they have paid their suppliers. They will also be able to choose to produce one annual return and an assessment will be made for monthly stage payments based on the previous year's VAT return. The Government hopes to introduce these measures from October 1, 1987.

There are now plans to introduce more changes in this year's finance bill. The administration of corporation tax is to be streamlined and a new scheme called "corporation tax pay and file" is to be introduced. A company will be required to pay corporation tax on a fixed date. It will be allowed 12 months from the end of its accounting period to submit its accounts and tax return. After that, there will be an automatic daily penalty. After a further 12 months, if the accounts still had not been submitted, there will be an additional 20% penalty of the tax due but not paid and on top of this, interest would be due on the tax not paid.

Although this new system will appear in this year's finance bill it will not be implemented until the Revenue's computers have been programmed to deal with it so there will be plenty of time for firms to adapt themselves to the new system.

Other changes that will be made are that PAYE and sub-contractor deduction schemes will be made more effective. At present there is no real incentive for an employer to pay over PAYE on time because there is no interest charge. As from April, 1988, interest will be charged for late returns.

The gravy days of the past are over, and even having a love affair with the local Collector of Taxes will not save businesses from the new penalties that will be churned out by irreversible and difficult to appeal against computers.

Big Brother would seem to have arrived bang on schedule, but not in quite

the way, or for the reasons that George Orwell forecast. The UK has a vast and rapidly growing business universe. There are nearly three million directors of eight hundred thousand limited companies and it is estimated there are upwards of a million sole proprietors and partners. These businesses generate unbelievable mountains of tax paperwork that the tax authorities simply cannot cope with except with the help of the implementation of very strict and arbitrary penalties.

Government thinking is dominated by the need to police this vast bureaucracy in a cheap and efficient way. As always the most efficient method is the most brutal, and it is the smaller company that usually suffers most.

The message for 1987 and beyond is clear. It is up to taxpayers to give the highest priority to comply with their VAT and Inland Revenue obligations. Failure to do so will lead to the destruction of businesses, and the government is well aware and prepared for the screams of anguish that will follow as a result. It will not take notice of them, because it has designed this particular rack with fiendish precision well aware that it will put its victims through great pain.

Those businesses that will suffer the most from this nightmarish new regime will include the innocent and the unwary. To avoid these new pitfalls it is more important than ever that firms ensure they understand the new rules, maintain proper records, and submit accurate returns on time.

If in any doubt, accountants should be consulted, or the Customs and Excise and Inland Revenue directly.

D by John McQueen