1

1 2

2 3

3 4

4 5

5 6

6 7

7 8

8 9

9 10

10 11

11 12

12 13

13 14

14 15

15 16

16 17

17 18

18 19

19 20

20 21

21 22

22 23

23 24

24 25

25 26

26 27

27 28

28 29

29 30

30 31

31 32

32 33

33 34

34 35

35 36

36 37

37 38

38 39

39 40

40 41

41 42

42 43

43 44

44 45

45 46

46 47

47 48

48 49

49 50

50 51

51 52

52 53

53 54

54 55

55 56

56 57

57 58

58 59

59 60

60 61

61 62

62 63

63 64

64 65

65 66

66 67

67 68

68 69

69 70

70 71

71 72

72 73

73 74

74 75

75 76

76 77

77 78

78 79

79 80

80 81

81 82

82 83

83 84

84 85

85 86

86 87

87 88

88 89

89 90

90 91

91 92

92 93

93 94

94 95

95 96

96 97

97 98

98 99

99 100

100 101

101 102

102 103

103 104

104 105

105 106

106 107

107 108

108 109

109 110

110 111

111 112

112 113

113 114

114 115

115 116

116 117

117 118

118 119

119 120

120 121

121 122

122 123

123 124

124 125

125 126

126 127

127 128

128 129

129 130

130 131

131 132

132 133

133 134

134 135

135 136

136 137

137 138

138 139

139 140

140 141

141 142

142 143

143 144

144 145

145 146

146 147

147 148

148 149

149 150

150 151

151 152

152 153

153 154

154 155

155 156

156 157

157 158

158 159

159 160

160 161

161 162

162 163

163 164

164 165

165 166

166 167

167 168

168 169

169 170

170 171

171 172

172 173

173 174

174 175

175 176

176 177

177 178

178 179

179 180

180 181

181 182

182 183

183 184

184 Transport's missing link

Page 21

Page 22

If you've noticed an error in this article please click here to report it so we can fix it.

A new report suggests that the growth in road freight is no longer directly influenced by underlying

economic grow-h. Louise Cole

looks at why this has happened — and what the development means for road transport operators.

EVERY COUNTRY needs economic growth and generally this has been a prime mover in stimulating the need for transport. The rub is that such growth, by increasing the need to move goods around. also makes huge demands on infrastructure and brings many costs in terms of increased congestion and pollution. Overall we cannot sustain economic growth that demands such a high price.

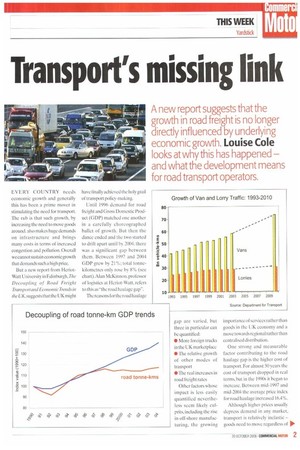

But a new report from HeriotWatt University in Edinburgh, The Decoupling of Road Freight :transport and Economic Trends in the UK,suggests that the UK might have finally achieved the holy grail of transport policy-making.

Until 1996 demand for road freight and Gross Domestic Product ((iDP) matched one another in a carefully choreographed ballet of growth. But then the dance ended and the two started to drill apart until by 2004, there was a significant gap between them. Between 1997 and 2004 GDP grew by 21%; total tonnekilometres only rose by 8% (see chart). Alan McKinnon, professor of logistics at He riot-Watt, refers to this as" the road haulage gap".

The reasons for the road haulage gap are varied, but three in particular can be quantified: • More foreign trucks in the UK marketplace • The relative growth of other modes of transport • The real increases in road freight rates Other factors whose impact is less easily quantified nevertheless seem likely culprits, including the rise in off-shore manufacturing, the growing importance of services rather than goods in the UK economy and a move towards regional rather than centralised distribution.

One strong and measurable factor contributing to the road haulage gap is the higher cost of transport. For almost 50 years the cost of transport dropped in real terms, but in the 1990s it began to increase. Between mid-1997 and mid-2004 the average price index for road haulage increased 16.4%.

Although higher prices usually depress demand in any market, transport is relatively inelastic — goods need to move regardless of price. However, recent government studies suggest that for every 1% rise in the real cost of road transport, the tonne-km figure declines by 0.1%.This accounts for 12% of the existing road haulage gap.

Just under 25% of the gap can be attributed to the shift to other modes. Until 1997 road had been increasing its share of the total tonne-km, but from then on rail started to inch forward,and water's share grew from 21% to 24%. leaving road freight slipping to 62.7% of the total market.

Roughly 25% of the road haulage gap can be accounted for by intermodal transport, although even when the growth in these sectors is factored in. there is still significant decoupling of tonnekm from GDP across all modes.

The effect of Our GDP base moving away from manufacturing and into services cannot be easily quantified, simply because it is impossible to separate those loads that are in support of services from the movement of manufactured goods. But commonsense dictates that the less we make, the less we will ship, and UK import figures for manufactured goods have grown steadily. Between 1997 and 2002 our intake of fabricated metal products grew by 284%; radios, TVs and communications equipment by 172%; vehicles by (39%; and published material by 83%.

However, it has to be acknowledged that these goods have to be moved at some point, whether it be by foreign hauliers or by UK hauliers on container work.

It would seem likely that higher imports underpin the higher levels of foreign vehicles in UK ports. which have grown from 52% in 1997 to75% in 2004.Unfortunately the work done by these trucks is not captured in UK tonne-km statistics and this distorts the overall picture.

Again cabotage figures can muddy the waters but one set of European statistics suggest that cabotage in the UK went from 79 million tonne-km in 1997 to 1.61bn tonne-km in 2003, following the 1998 liberalisation (see panel).

If figures from foreign hauliers were included in the tonne-km assessment the gap would narrow by almost 30% — meaning that overall there is a greater demand for road transport than the graph opposite. But despite this, the ratio of tonne-km (including foreign trucks) to GDP declined by 11%.

The average journey length has also stabilised: until 1997 there was a gradual rise to 93km, but this has dipped and held steady since. One related factor could be the move to more local sourcing, with the centralisation seen in distribution having reached its logical conclusion and more regional distribution asserting itself once more.

There is evidence more freight is being transported by vans and not trucks. which can again distort the figures as activity data on vehicles under 3.5 tonnes isn't captured.

The use of these vehicles may be driven by a need for local deliveries, consolidation centres and justin-time systems. It is mirrored by another implicated factor: the increasing efficiency of supply chain logistics.

The report casts doubt on the validity °fusing G D P as an accurate base for estimating freight growth because the service proportion of the economy is set to keep growing and we don't know what impact this will have on freight. So while economic indicators for specific industrial sectors might still be relevant,overall G DPis no longer a good indicator of demand for the UK road transport industry.

I• To see the whole report go to the Logistics Research Centre website: .. wwwsml.hw.ac.uldlogistics

The impad of foreign operations

There is much conflicting data surrounding the impact of foreign trucks on UK roads. The Burns Inquiry said it had a regional, port-based effect, but RHA chief executVe Roger King claimed a market penetration of 25% (CM 14 September). The model he uses involves stripping out all of the operations on which cabotage could have no impact to find the real impact on the remainder of the industry. The Decoupling of Road Freight Transport and Economic Trends in the UK states that the activities of foreign trucks have only been surveyed twice, in 2000 and 2003. By assuming a direct correlation between the number of foreign vehicles and the tonne-km they account for, the report suggests the following: • Foreign trucks ran five bn tonne-km on UK legs of international journeys between 1997 and 2003

• Total tonne-km carried by UK hauliers declined by 28% between 1997 and 2003

• UK international haulage dropped by up to 1.4bn tonnekm between 1997 and 2003