1

1 2

2 3

3 4

4 5

5 6

6 7

7 8

8 9

9 10

10 11

11 12

12 13

13 14

14 15

15 16

16 17

17 18

18 19

19 20

20 21

21 22

22 23

23 24

24 25

25 26

26 27

27 28

28 29

29 30

30 31

31 32

32 33

33 34

34 35

35 36

36 37

37 38

38 39

39 40

40 41

41 42

42 43

43 44

44 45

45 46

46 47

47 48

48 49

49 50

50 51

51 52

52 53

53 54

54 55

55 56

56 57

57 58

58 59

59 60

60 61

61 62

62 63

63 64

64 65

65 66

66 67

67 68

68 69

69 70

70 71

71 72

72 73

73 74

74 75

75 76

76 77

77 78

78 79

79 80

80 81

81 82

82 83

83 84

84 85

85 86

86 87

87 88

88 89

89 90

90 91

91 92

92 93

93 94

94 95

95 96

96 97

97 98

98 99

99 100

100 101

101 102

102 103

103 104

104 105

105 106

106 107

107 108

108 109

109 110

110 111

111 112

112 113

113 114

114 115

115 116

116 117

117 118

118 119

119 120

120 121

121 122

122 123

123 124

124 125

125 126

126 127

127 128

128 129

129 130

130 131

131 132

132 133

133 134

134 135

135 136

136 137

137 138

138 139

139 140

140 141

141 142

142 143

143 144

144 145

145 146

146 147

147 148

148 149

149 150

150 151

151 152

152 153

153 154

154 155

155 156

156 157

157 158

158 159

159 160

160 161

161 162

162 163

163 164

164 165

165 166

166 167

167 168

168 169

169 170

170 171

171 172

172 173

173 174

174 175

175 176

176 177

177 178

178 179

179 180

180 How EXPORTS ARE

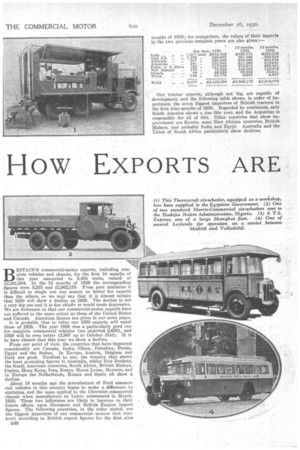

Page 110

Page 111

Page 112

If you've noticed an error in this article please click here to report it so we can fix it.

DEVELOPING

A Survey of the World's Markets for Commercial Vehicles, Motor Chassis and Tractors, Showing Their Relative Importance to the British Manufacturers

BRITAIN'S commercial-motor exports, including complete vehicles and chassis, for the first 10 months of this year amounted to 5,456 units, valued at/2,261,504. In the 12 months of 1929 the corresponding figures were 8,223 and 12,962,179. From past statistics it is difficult to single out any season as better for exports than the others, so we may say that it is almost certain that 1930 will show a decline on 1929. The decline is not a very big one and it is due chiefly to world trade depression. We are fortunate in that our commercial-motor exports have not suffered to the same extent as those of the United States and Canada. American figures are given in our news pages.

It is probable that in value our 1930 exports will equal those of 1928.. The year 1929 was a particularly good one for complete commercial vehicles (we exported 2,636), and 1930 will be even better (2,907 up to October 31st). It is in bare chassis that this year we show a decline.

From our point of view, the countries that have improved considerably are Canada, India, China, Palestine, Persia, Egypt and the Sudan. In Europe, Austria, Belgium and Italy are good. Needless to say, the country that shows the least promising figures is Australia, whilst New Zealand, the South American countries, South Africa, British Malaya, Ceylon, lIong Kong, Iraq, Kenya, Sierra Leone, Morocco, and in Europe the Netherlands, Russia and Spain all show a decline.

About 18 months ago the manufacture of Ford commercial vehicles in this country began to make a difference to statistics, and the same applied to the Chevrolet commercial chassis when manufacture at Luton commenced in March, 1930. These two influences are likely to increase in their future effects upon European and British Empire import figures. The following countries, in the order stated, are the biggest importers of our commercial motors (not tractors) according to British export figures for the first nine

, E48 months of 1930; for comparison, the values of their imports in the two previous complete years are also given:— Our tractor exports, although not big, are capable of development, and the following table shows, in order of importance, the seven biggest importers of British tractors in the first nine months of 1930. Regarded by continents, only South America shows a rise this year, and the Argentine is responsible for all of this. Other countries that show improvement are Russia, some East African countries, British Malaya, and probably India and Egypt. Australia and the Union of South Africa particularly show declines: For comparison the figures for the 12 months of 1929 are also given in this table :— We find that special contracts for buses, etc., play ducks and drakes with the commercial-motor export figures, this being especially noticeable in European countries.

The Irish Free State is by far our best customer in Europe and the second best market in the world. After settling her political troubles, Ireland commenced to consume commercial motors as never before. The number of complete vehicles supplied by Britain rose steadily from 117 in 1925 to 352 in 1928, and then jumped to 1,304 in 3929, the average value at the same time dropping from about 1451 in 1928 to about £154 the next year. It is a ease where figures tell their own story, and the transfer of manufacture of Ford chassis to the Manchester works, of course, had much to do with it. The year 1930 shows a continued advance in cheap vehicles, the number to September being 1,108. Last year the country took 292 British chassis against :170 in the first nine months of 1930.

The Channel Islands present a steadily increasing market, which took 214 vehicles and 15 chassis last year, and has, to September, 1930, taken 161 vehicles and 3 light chassis, the total value being £34,909. This becomes our second best European market in place of the Netherlands.

In January-September, 1930, Sweden has taken 6 British vehicles, averaging about £1,000 each, and 41 chassis, the total value of imports being £14,536 as compared with 1 vehicle and 25 chassis (gross value £20,950) in 1929. This places Sweden in the third place in Europe. Up to September Greece has taken 13 vehicles (£7,468) and 9 light and 18 heavier chassis, compared with 19 expensive vehicles and 11 chassis in the whole of 1929. Belgium and Austria have both taken a few expensive machines this year, the values being £12,071 and £7,667 respectively.

Spain, after taking 122 chassis and 26 vehicles in 1929 (albeit at low average value), has in January-September, 1930, taken only 5 cheap vehicles and 7 light and 9 heavier chassis. The fall in the exchange rate is reckoned to be largely responsible for the position there. The Netherlands, which, in 1929, constituted our second best European market, taking 31 vehicles and 383 chassis, has to September this year taken only 18 vehicles and 6 chassis.

Czecho-Slovakia has in these nine mouths taken but 1 cheap vehicle and 14 chassis (total £2,775), as compared with 1 vehicle and 42 chassis (18,822) last year. Poland's imports of 26 units (£7,368) compare with 37 units (f8,741) in the whole of 1929. Another country worth mentioning this year is Roumania (33 units, £7,966). With regard to our tractor exports these nine months to Europe, Russia has become pre-eminent with 84 agricultural machines, valued at £25,302, and in the same period France has taken 25 machines (£4,858) and Italy 12 machines (12,370), as against 27 machines (18,931) and 81 machines (£12,244) in the whole of 1929. The 173 tractors (£45,953) shipped to Europe in January-September, 1930, compare with 234 (159,006) in the 12 months of 1929.

Turning now to the American continent, Canada shows a great improvement. It is twice as irnporlant a market for British commercial vehicles and chassis as the Channel Islands, although when the areas are compared this statement seems rather absurd. In January-September, 1930, Canada took 2 British vehicles (£1,238) and 92 chassis, all of the chassis except 1 weighing over 28 cwt., and their value averaging about £700, so that Canada's total imports are worth £68,684, compared with 150,698 in the whole of 1929. The United States are of no value to us.

As for Central America, our total exports these nine months amounted to 37 units (£12,694), showing a bad drop on the 12 months of 1929 (64 units, 127,395). Jamaica, Trinidad and Tobago and Salvador are the most promising Central American countries.

Temporary Argentine Troubles.

The Argentine is by far our best South American customer and one of the most hopeful of all our markets. Of 63 British vehicles taken by South America in 1929, 33 went to the Argentine, and of 931 chassis, the Argentine's share was 785. The average value of the vehicles last year was £687. In January-September, 1930, the Argentine has taken 28 vehicles at an average value of nearly £1,600, a very high figure. In chassis, 1930 is not nearly so good. Of the 785 chassis taken last year 464 were light machines, mostly of the 30-cwt. type, and the heavier types totalled 321. The average value of the 785 chassis was about £370.

In January-September, 1930, however, only 213 chassis went to the Argentine, 18 of these being light machines and 195 weighing over 28 cwt. The average value of the heavier chassis was £422. This regrettable position is largely due to the fall in value of the peso and severe, but temporary, internal troubles. There is no need for discouragement, as we explain in a separate article in this issue.

Next to the Argentine comes Brazil, but 1930 shows a setback here also. Last year Brazil took 17 vehicles at about £1,250 each and 73 chassis of average value about £400, In January-September, 1930, only 7 vehicles have been taken, their average value being .about £1,000. The number of chassis is 16, of which 9 wdre light machines.

Chile, a much smaller market, is also lower this year, having taken 6 chassis (£3,519) as against 15 chassis

(£9,525) in the whole of 1929. Venezuela has taken 7 ex

pensive vehicles (£10,252) and no chassis, compared with 1 vehicle (12,400) and 10 costly chassis (averaging £1,308 each) in 1,929. Uruguay is exceptional, having taken 5 vehicles (£5,396) and 10 chassis, of which 8 are heavy types averaging £000 each, as compared with 7 vehicles and 39 chassis of low average cost last year. The only other South American country of interest this year is Peru, with 6 vehicles and 6 chassis, aggregating 12,840.

In January-September, 1930, the Argentine has taken 9 agricultural and 24 industrial tractors from Britain (120,278), bringing her into third position in the world from our point of view. The rest of South America has only taken 12 tractors, making a total of 45 machines for the southern continent, as against 44 in the whole of 1929-an indication that tractor makers should watch the Argentine.

In Asia, India leads by far, and the figures for 1929 and 1930 appear very good. In January-September, 1930, India has taken 932 vehicles of average value £789 and 285 chassis of average value £284, 156 of the chassis weighing over 28 cwt. These figures compare -with 494 vehicles of high average value• and 311 chassis (average £416) in 1929, 1928 figures being considerably lower. The civil demand has suffered a definite setback owing to political disturbances and the figures are buoyed up by orders for the Government.

Persia in the past few months has sprung into the second position in Asia and eighth in the world from the British point of view, having in January-September, 1930, taken 100 vehicles (average £524) and 46 chassis. The figures compare with 2 vehicles and 40 chassis in 1929.

British Malaya is thus ousted from the second position in Asia, and this.year looks like showing a considerable drop in imports. Our exports comprise 27 vehicles (average 1500), 31 light chassis, and 60 heavier chassis (averaging about £400). The total of 118 units (£43,437) compares with 229 units .(£82,648) in the 12 months of 1929.

E50 Returning to the Near East, Palestine shows rather a remarkable improvement this year, having taken 63 vehicles at an average value of about £500, also 25 cheap chassis, the aggregate cost being £35,807 compared with £5,557 in 1929 (12months). The only other Asiatic market which shows in a favourable light is China, which, despite all its strife and famines, has taken 3 British vehicles and 47 chassis ; 34 of the chassis are of the heavier te averaging in value about £600. The figures compare with 12 vehicles and 35 chassis in 1929, which, incidentally, showed no great departure from previous years.

Ceylon and Hong Kong, both under British rule, show bad declines this year. Ceylon took only 7 vehicles and 10 chassis (£4,919) in the nine months, compared with 27 vehicles and 84 chassis (£33,056) in 1929, whilst Hong Kong has taken 5 vehicles and 19 chassis (£11,268), compared with 21 vehicles and 50 chassis (£19,057) last year.

The Dutch East Indies are not promising, their total consignments coming to £8,221, as against £13,016 in the whole of 1929; Java took 2 vehicles (£1,188) and 21 chassis (£6,470). French-Indo China and Siam do not count this year and Japan has taken only 11 units (£3,171). Syria, Iraq, Arabia and Port of Aden form but a small market, although last year Iraq was worth £21,086 to us. No other countries in Asia need mentioning.

This year Asia has accounted for 40 tractors (112,139), of which 32 went to India.

The Depression in Australia.

The position in Australia is revealed by our exports in January-September, 1930, which come to only 13 vehicles at about 1600 each and 494 chassis, averaging nearly 040. In 1929 Australia took 34 vehicles averaging nearly £1,000 apiece and 1,287 chassis. The figures show a serious decline since 1925,1926 and 1927. New Zealand has taken 19 vehicles (£8,394) and 151 chassis (£64,668), as compared with 21 vehicles and 412 chassis in 1929. The British hold

on this market was showing a marked improvement at the beginning of this year, and, given better trade conditions, New Zealand promises well. As regards tractors, Australia. has taken 71 (£26,548), compared with 106 (£41,797) last year, and New Zealand 1 machine compared with 24.

This brings us to the African Continent, which last year was about as valuable to us as Australia, business coming to about £456,000, exclusive of tractors, and comprising 187 vehicles and 864) chassis, as against 153 vehicles and 319 chassis, aggregating about 1.232,000 in January-September this year. The Union of South Africa is the most impor tant African country and our fifth best world market, yet it shows a decline in 1930, having taken in January September 36 vehicles and 147 chassis (1.117,699), as compared with 49 vehicles and 467 chassis (£275,873) in 1929. Up to last year the vehicle orders compared well with any of the previous four years, except 1927, and the chassis figures showed a steady advance. It would surprise some to learn that Nigeria is the second most important African country, well surpassing Kenya and

Egypt in 1929 and 1930, when the imports comprised 32 vehicles and 62 chassis (04,310), as against a vehicles and 37 chassis (£23,210) in Suay-September, 1930. As regards other West African countries, the Gold Coast is fourth in Africa and has taken 22 vehicles (£12,824) and " 21 cheap chassis, as compared with 24 vehicles (£9,055) and 44 chassis (£13,420) in 1920. Sierra Leone, which took 17 vehicles last year (£7.768), is worth nothing so far.

Third place in Africa, which was held by Kenya last year, is now occupied by Egypt, which has taken 11 vehicles and 37 chassis (121,873), an improvement on 1929, when our exports were 29 vehicles and 42 chassis (£21,294). The Anglo-Egyptian Sudan is fifth African country this year,

having taken 15 vehicles at the high value of £15,856, as well as 8 chassis, a considerable improvement on last year. The sixth country in Africa is Kenya, with 8 vehicles (14,839) and 12 chassis, averaging about 1480. The imports of Tanganyika, Zanzibar and Pemba, Uganda and Nyassaland come to respectively 12,302,1.1,200, 1979, 11,016. Northern and Southern Rhodesia have taken 13 units (£5,232), and Portuguese East Africa has accounted for 11 units (15,883). Portuguese and French West Africa, Morocco, Algeria and the Belgian Congo have done us no good this year.

With regard to tractors, Africa has this year taken 58 (£18,578), as against 102 (£30,753) in the whole of 1929. Of the 1930 figures the Union of South Africa accounts for 16 (1.6,266), Egypt for 17 (13,945) and Portuguese East Africa for 12 (£3,357). The last-named deuntry is becoming valuable. Kenya his taken 3 tractors costing £1,507 and one £888 machine has gone to Zanzibar.