1

1 2

2 3

3 4

4 5

5 6

6 7

7 8

8 9

9 10

10 11

11 12

12 13

13 14

14 15

15 16

16 17

17 18

18 19

19 20

20 21

21 22

22 23

23 24

24 25

25 26

26 27

27 28

28 29

29 30

30 31

31 32

32 33

33 34

34 35

35 36

36 37

37 38

38 39

39 40

40 41

41 42

42 43

43 44

44 45

45 46

46 47

47 48

48 49

49 50

50 51

51 52

52 53

53 54

54 55

55 56

56 57

57 58

58 59

59 60

60 61

61 62

62 63

63 64

64 65

65 66

66 67

67 68

68 69

69 70

70 71

71 72

72 73

73 74

74 75

75 76

76 77

77 78

78 79

79 80

80 81

81 82

82 83

83 84

84 85

85 86

86 87

87 88

88 89

89 90

90 91

91 92

92 93

93 94

94 95

95 96

96 97

97 98

98 99

99 100

100 101

101 102

102 103

103 104

104 105

105 106

106 107

107 108

108 109

109 110

110 111

111 112

112 113

113 114

114 115

115 116

116 117

117 118

118 119

119 120

120 121

121 122

122 123

123 124

124 125

125 126

126 127

127 128

128 129

129 130

130 131

131 132

132 133

133 134

134 135

135 136

136 An accountant's-eye-view of the small haulier's

Page 49

Page 50

Page 51

Page 52

If you've noticed an error in this article please click here to report it so we can fix it.

financial problems by John Darker EVERY SIZE of road haulage company is facing severe difficulties today, but the problems of the smallest firms, operating from one to five vehicles, are particularly grave.

With less "bargaining" strength than the medium and large-sized haulage contractors, whose vehicles may be indispensible to their customer firms by. virtue of proximity of operating base, specialized vehicles or knowledgeable drivers, the "small fry" can easily go to the wall in a trading slump.

I recently discussed some of the financial problems of small hauliers with a West Country accountant, Mr A. B. Brown, who has over many years acquired considerable knowledge of this particular field.

Visits to hauliers

Mr Brown's experience since 1947 with West Country hauliers began with advice on the figures to be submitted to support licence applications. He is a shrewd observer of the industry and before giving hard advice he likes to see for himself, by visits to hauliers, just what the true background is. Some hauliers' accounts simply do not match up with their "life-style". Where it is obvious that too much money is being taken out of a small business for its continued viability or growth, he tells the person concerned the truth. "Some take notice," said Mr Brown, "others soon find themselves in difficulty and eventually withdraw from the industry."

A great many of the one to three vehicle operators are over-obsessed with the tax situation. They compare notes with fellow-operators and if one pays more tax than another they rush to the accountant to ask for an explanation. So often the accountant is blamed, but it's a question of a business run profitably or otherwise, coupled with the personal circumstances of the proprietor.

Now that the traditional remedy for low haulage rates is scarcely possible today — overloading and excessive driving hours — many small hauliers unrealistically look to their accountant for some miraculous juggling of the figures to provide a worthwhile profit. Life is not that easy! The haulier inust look for economies in operational costs.

Eager salesmen

Currently, said Mr Brown; small hauliers are being pressed by commercial vehicle salesmen to renew vehicles older than four years. The sensible hauliers ask advice before they commit themselves. But many small men swallow the salesman's bait about tax relief. They are told that the cost of the vehicle can be offset against profits in a single year. When this is so the relief from tax is only at the rate applicable to the particular haulier. Basic rate is 33 per cent. The question arises: Is it economic to spend that other 67 per cent to save 33 per cent to the Revenue?

"There are so many different circumstances to be considered," said Mr Brown. "A haulier could be heavily borrowed from his bank, etc. Family circumstances vary."

What does Mr Brown advise in this common situation? He advises hauliers to look at their existing fleet of vehicles. 1:1 Are some, or all, fully paid for? El What is the mechanical condition of each vehicle? 1:1 Who does the vehicle maintenance bearing in mind the huge advantage when a small firm does the hulk of its own maintenance in the evenings or at weekends?

The man who does his own repairs will save the profits that a vehicle repair specialist would get and in addition, less down-time — and hence more profitable working days — are possible.

Mr Brown is not opposed to a small haulier doing fairly detailed costing of his operations, but he stresses that the very small firm must not get bogged down on costing analysis. The aim should •be to maximize vehicle availability since no customer firm can be expected to took favourably on an unreliable haulier whose vehicles, for any reason, are not on offer when work is available.

Of course, there are good organizers of five-vehicle fleets who earn more from their organizing than they would as a driver in the firm. But today it is less easy to "play the market" for the best rated jobs. Small hauliers must take what work is available at the prevailing rates, and use their intelligence to relate the return on different classes of traffic in terms of profits.

"Some hauliers think they will do better on long-distance jobs paying a fairly high rate per tan, but there can be much more profit in a series of short runs, and possibly less wear and tear as well."

Mr Brown, who is closely associated with quarry operations as well as with the hauliers undertaking quarry work, points out the significance of competitive haulage rates to the quarry industry. Some quarries with their own fleets of vehicles are now making less use of sub-contractors, with dire effects on a number of small operators.

What can a small haulier do to help himself — and his accountant — in present circumstances?

"Some hauliers," said Mr Brown, "are very careless about out-of-pocket expenses. Business entertainment — other than for exports — is not an allowable expense. The only sensible rule is for all expenses connected with the business to be recorded. The accountant will know what is legitimately chargeable and what is not."

Attractions of status

Many small hauliers are tempted to form themselves into a limited company, but Mr Brown is not unreservedly in favour of this though he understands the attraction of a managing director title which corporate status provides. "1 always ask why a small haulier is so attracted by the limited company idea. Some say, 'To protect my home'. But that is not a good, or valid, reason. Why protect your personal assets at other people's expense? Unless a small haulier is quite confident about the viability of his business he should not imagine that trading as a limited liability company offers any solution to business worries."

And Mr Brown warns that mediumsized haulage businesses which are continued from page .47 limited companies can easily get into trouble today if their customers do not or cannot pay their bills. .

He stresses that the small man who persists in trading as a limited company will almost certainly — unless he has adequate personal capital — have to offer as security for a bank or other loan his own home or personal assets. This partially defeats his main reason for wanting to be "limited." The relative ease of forming a limited liability private company — the market rate for this is in the region of £80 to £100— should not induce small hauliers to trade under this banner without very good reasons.

I asked Mr Brown if he saw any advantage of a trading title obtainable V registration under the Business \lames Act. He felt the small man could lot readily disguise his smallness in this fashion. Far better trade in one's own lame initially.

Best lorry to buy

On the question of the type of vehicle :o buy, when purchase is justifiable on lusiness grounds, Mr Brown felt that most very small hauliers would do well :o acquire a mass-produced, popular .ype of lorry rather than go in for the nore specialized "quality" products. 'You must look at this from the angle of he possible vehicle earnings in relation o carrying capacity. Of course, an :xpensive vehicle may last longer, but inless it is producing more revenue each week you will be incurring more capital )utlay to pay for it."

Does it ever pay to keep a substantial )ank balance, yielding interest at 9 per ;ent, or whatever, when a higher yield nay be possible elsewhere? Mr Brown hought it could make sense in the short :un to keep a substantial bank balance if new vehicle must soon be purchased or f — as can be — it is desirable to acquire 'resh premises or improve existing. k part from improved operational idvantages land and premises provide worthwhile assets to a business which :ould be of great benefit in times of diffi:ult trading.

The many changes in the law in recent rears have been confusing to business nen. It used to be possible for directors o take a tax free loan from their :omPany, but today such a loan is axable — it is treated as income in the 'ear in which it is taken. Relief is ivailable when the repayment is made. he amount of tax payable is according o the individual's personal liability for he year in question.

It can be very costly to borrow money rom a company for personal use. The iquidity of the business must suffer if his is done, and there is no way round he personal and cOmpany tax laws to disguise what is really a "milking" operation which could damage the viability of a business.

Much of Mr Brown's advice has a traditional ring about it! Some of the most successful hauliers that he knows excel in not spending money. He quotes one haulier friend who says: "I never spend a shilling if I can save one."

While the larger fleet operators must expect to replace their fleets on a phased basis, annually, the one or two-vehicle operator must decide whether his vehicle(s) is economic. "The most you can lose with a vehicle worth £800 is the capital element, subject to the running costs. Depreciation at the rate of 25 per cent a year is not a heavy expense. But if you buy a vehicle for £3,000 or £4,000 the depreciation figure is much higher. The small man who continues to operate the vehicle worth £800 for another two years may be able to get £300 or £400 as part exchange price even then.

"If a new vehicle had been purchased, a lot more money would have had to be earned to pay for the outgoings."

Mr Brown concedes that haulage in the quarry industry is a tough job for the small operators. Other types of goods traffic can be more lucrative. Some operators of a single box-type vehicle do very well. Indeed, some owneroperators have a better return with a single vehicle than others with two vehicles — because of the high driver's pay necessary with an employed driver.

What happens when an employed driver goes into business on his own account? He will pay tax under PAYE arrangements from April 6 until the day he operates his own business. Profits of the first year are apportioned for the part-year to April 5 next. Trading results are worked out for one year from date of commencement of trading. It frequently happens that small hauliers allow their annual accounts to get in arrear, and this means that the figures are virtually useless for control purposes when completed.

The account books should normally be sent to the accountant for auditing within six weeks of the end of the trading year. The accountant can then bring to the operator's notice items of excessive expenditure whether it is on direct running costs or overheads.

It cannot be stressed too plainly that the best accountant can do nothing to protect a businessman from his own folly, or from bad trading or operating practices if the full records of the business are not produced in time. A careful audit of the books can often reveal the area of operations where the losses are occurring. "The only people who will press hard for trading figures to be produced will be the Inland Revenue, but the IR may not worry until the accounts are perhaps two years in arrear. By that time a business in a bad way may be doomed,."

Auditor's instinct

In auditing, not every item will be scrutinized; some of the detail is subject to a percentage check, though the auditor's instinct will tell him what it is necessary to probe and if necessary ask for more information. Tax inspectors, too, may compare one haulier's figures with another's. It often happens that a small haulier earning a gross revenue of, say, £9,000 against expenses of £4,000 will be compared with a firm grossing' £10,000 on expenses of £3,000. Such figures could be explained by the more profitable firm undertaking its own vehicle maintenance.

Mr Brown says of leasing deals that if it is profitable to the leasing company it must surely be more progitable for the haulier to buy his own vehicle. The hire purchase versus leasing dilemma is a question of availability of capital. Hauliers are best advised to consult their own accountants on this aspect of purchase.

Mr Brown generally supports the quarry industry's accounting services to small hauliers as this ensures the job is done more quickly. Of course, the haulier should check that all his journeys have been recorded and paid for.

To those who would insist that every job undertaken should be profitable, Mr. Brown thinks this is not sane advice for the small haulier. "It's results over the year that count. Anyone bothering about the profitability of each trip will be in for a proper headache. Some loads will only pay the driver's wages, but the owner driver earning £50 for a week's work will regard this reasonably enough as his wages. It is better to maintain the goodwill of your customers by accepting some low-rated traffic than have the vehicle idle. Better to only 'break even' in covering wages than refuse work, although this must not be overdone."

Inaccurate information

Statistics are often based on inaccurate information obtained from a variety of sources. The small man must do the best he can with the rates his customers can afford to pay, ploughing back as much as he can spare to make his business more soundly based. "Those who take more out of the business than it is earning can only look forward to a business failure." BUYING a coach is very different from buying a car or lorry. The initial cost of a car or lorry is swiftly written down to nearly zero, whereas a coach is sure to hold its price for many years. Although this makes buying a secondhand vehicle expensive, the owner has a solid investment that he knows will command a good price when the time comes to replace it. This can, of course, make buying by hire purchase easier as the finance company can be sure of having something of value left to them should the purchaser default on the agreement.

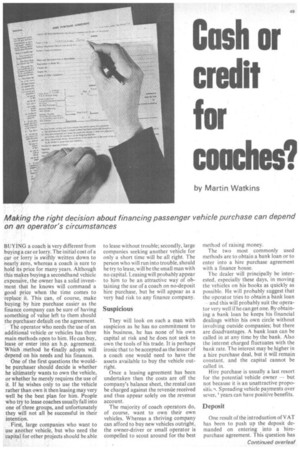

The operator who needs the use of an additional vehicle or vehicles has three main methods open to him. He can buy, lease or enter into an h.p. agreement. Which method he finally adopts will depend on his needs and his finances.

One of the first questions the wouldbe purchaser should decide is whether he ultimately wants to own the vehicle, or whether he merely requires the use of it. If he wishes only to use the vehicle rather than own it then leasing may very well be the best plan for him. People who try to lease coaches usually fall into one of three groups, and unfortunately they will not all be successful in their intention.

First, large companies who want to use another vehicle, but who need the capital for other projects should be able to lease without trouble; secondly, large companies seeking another vehicle for only a short time will be all right. The person who will run into trouble, should he try to lease, will be the small man with no capital. Leasing will probably appear to him to be an attractive way of obtaining the use of a coach on no-deposit hire purchase, but he will appear as a very bad risk to any finance company.

Suspicious

They will look on such a man with suspicion as he has no commitment to his business, he has none of his own capital at risk and he does not seek to own the tools of his trade. It is perhaps ironic that to be accepted as the lessor of a coach one would need to have the assets available to buy the vehicle outright.

Once a leasing agreement has been undertaken then the costs are off the company's balance sheet, the rental can be charged against the revende received and thus appear solely on the revenue account.

The majority of coach operators do, of course, want to own their own vehicles. Whereas a thriving company can afford to buy new vehicles outright, the owner-driver or small operator is compelled to scout around for the best method of raising money.

The two most commonly used methods are to obtain a bank loan or to enter into a hire purchase agreement with a finance house.

The dealer will principally be interested, especially these days, in moving the vehicles on his books as quickly as possible. He will probably suggest that the operator tries to obtain a bank loan — and this will probably suit the operator very well if he can get one. By obtaining a bank loan he keeps his financial dealings within his own circle without involving outside companies; but there are disadvantages. A bank loan can be called in at any time by the bank. Also the interest charged fluctuates with the bank rate. The interest may be higher in a hire purchase deal, but it will remain constant, and the capital cannot be called in.

Hire purchase is usually a last resort for the potential vehicle owner but not because it is an unattractive propositiLl. Spreading vehicle payments over sever, ' years can have positive benefits.

Deposit

One result of the introduction of VAT has been to push up the deposit demanded on entering into a hirepurchase agreement. This question has

Continued from page 49

been discussed in the CM publication Yl/hai a haulier needs to know. Briefly, the purchaser can reclaim the entire VAT payable on the purchase after he has paid the initial deposit. If the deposit he pays is small he can therefore be repaid an equal or perhaps greater amount from VAT.

This is not popular with the finance houses as the result can be that he has paid no deposit in real terms and thus has no stake in the vehicle. He has obtained the vehicle for no overall cash outlay and has thus little commitment to continue the payments. To get around this point the finance house demand a deposit large enough to ensure that after VAT has been repaid the purchaser has still a considerable amount of money tied up in the vehicle.

The terms of hire-purchase agreements for the sale of cars are subject to Government control. This does not apply to lorries and coaches; the finance company is free to fix its own term and deposit arrangements.

Before a finance house agrees to any hire-purchase sale it will satisfy itself that the merchandise, in this case the coach, will in fact be of value throughout its life. This is where coach purchasers can score over those buying cars or lorries. The value of any coach returned in default will be considerable, and this, of course, helps to keep rates initially low.

Most hire purchase agreements for the sale of coaches cover periods of either 24 or 36 months. However, 48month agreements can sometimes be arranged.

Unbiased

When buying a coach the purchaser can take the advice of his dealer knowng it to be reasonably unbiased. It is not of any real monetary advantage to the iealer to recommend one particular -nethod of finance. The usual practice .hese days is for the dealer to forsake my commission due to him in order to ;ubsidize the transaction. He will make us money on the cash price of the coach vhich will be paid to him by the finance eompany when the vehicle is delivered o the buyer.

The purchaser will not be the legal owner of the coach until the last payment is made. This payment contains the option to purchase which is an adiitional fee of £2.

Obtaining a bus-grant — providing the operator is entitled to one — is .itraughtforward if a coach is bought on credit, provided a certain procedure is followed. This is necessary as the grant is paid only to the legal owner of a vehicle. The best method is probably to obtain a loan for the total purchase price of the coach, say £10,000. The operator