'YOU NEED TO KNOW ABOUT

Page 56

Page 57

If you've noticed an error in this article please click here to report it so we can fix it.

RECORDING DAILY COSTS

AND REVENUE

Reg P. Block "COSTING" of itself is a repetitive, time-wasting arithmetical chore unless it can be tailored to assist the'newcomer or existing management in decision taking. To achieve this aim it is necessary to relate performance to costs in order to produce a unit cost; eg, cost per ton, cost per job. In so doing the operator will have gone beyond "costing" as such and into the more sophisticated area of management accounting, for which I suggest costing is simply a prerequisite.

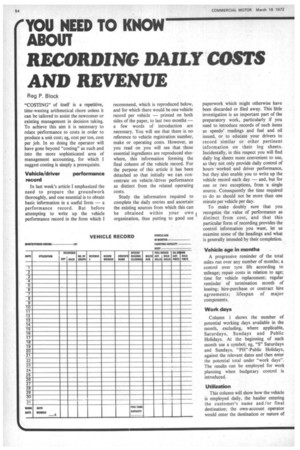

Vehicle/driver performance record In last week's article I emphasized the need to prepare the groundwork thoroughly, and one essential is to obtain basic information in a useful form — a performance record. But before attempting to write up the vehicle performance record in the form which I recommend, which is reproduced below, and for which there would be one vehicle record per vehicle — printed on both sides of the paper, to last two months — a few words of introduction are necessary. You will see that there is no reference to vehicle registration number, make or operating costs. However, as you read on you will see that these essential ingredients are reproduced elsewhere, this information forming the final column of the vehicle record. For the purpose of this article it has been detached so that initially we can concentrate on vehicle/driver performance as distinct from the related operating costs.

Study the information required to complete the daily entries and ascertain the existing sources from which this can be obtained within your own I organization, thus putting to good use

paperwork which might otherwise have been discarded or filed away. This little investigation is an important part of the preparatory work, particularly if you need to introduce records of such items as speedo' readings and fuel and oil issued, or to educate your drivers to record similar or other pertinent information on their log sheets. Incidentally, in this respect you will find daily log sheets more convenient to use, as they not only provide daily control of hours worked and driver performance, but they also enable you to write up the vehicle record each day — and, but for one or two exceptions, from a single source. Consequently the time required to do so should not be more than one minute per vehicle per day.

To make doubly sure that you recognize the value of performance as distinct from cost, and that this particular form of recording provides the control information you want, let us examine some of the headings and what is generally intended by their completion.

Vehicle age in months

A progressive reminder of the total miles run over any number of months; a control over tyre life according to mileage; repair costs in relation to age; time for vehicle replacement; regular reminder of termination month of leasing; hire-purchase or contract hire agreements; lifespan of major components.

Work days

Column 1 shows the number of potential working days available in the month, excluding, where applicable, Saturdays, Sundays and Public Holidays. At the beginning of each month use a symbol; eg, "S" Saturdays and Sundays, "PH"-Public Holidays, against the relevant dates and then enter the potential total under "work days". The results can be employed for work planning when budgetary control is introduced.

Utilization

This column will show how the vehicle is employed daily, the haulier entering the customer's name and/or final destination; the own-account operator would enter the destination or nature of work, for example loth would enter why the vehicle waq 'irking against the appropriate dates — such as: in for inspection, servicing repairs, no work or no driver. This record enables the operator to calculate the monthly percentage of time gainfully employed and furthermore provides a permanent record and ready reference to vehicle use; and, for a DoE examiner, the intervals between inspections, servicing and attention to defects.

Delivered-out/back In column 3 we enter tonnage, gallonage, cubic metres, parcels delivered /collected or whatever measure is appropriate to the yardstick on which you base your costs or charges.

Number of drops In this column show the drops made, to which should be added the number of collections in order to determine the number of "calls made". This will assist the work planner to estimate the time required to complete the day's work within the legal hours limit, with due regard to the optimum number of calls in relation to the trip mileage.

Revenue

The haulier should enter (in column 5) to the nearest £ the daily revenue earned per vehicle — excluding VAT invoiced — but when collections are made on any one day for next-day delivery, the revenue should be bracketed over the two days employed. In these operations it is essential to bear in mind that the delivered rate to charge must cover the cost plus profit for the two days — and possibly two vehicles — employed. Where the own-account operator can enter the total sales value of the goods or services sold per vehicle /day it will provide him with a very useful statistic, as we shall see at a later stage.

Hours worked Enter in column 6 hours actually worked, excluding deemed time or guaranteed hours. It serves no useful purpose to enter 11 hours per day for a five-day week irrespective of the content of each day's work, as it precludes the work planner from allocating a fair day's work — as he has estimated — for a fair day's pay. Although the tendency is to give drivers staff status with a guaranteed weekly pay packet, which I applaud, for work performance and cost accounting it is hours actually worked that are needed here.

Driver's name To a great extent this entry is self-explanatory but note its further uses; ie. extent of labour turnover; comparative performances in output and time taken; comparative uses of fuel and oil; accident history and incidence of breakdowns.

Speedo reading (closing) and miles run

Before you introduce a performance/ costing system ensure that all the mileage recorders on vehicles are in working order, and if not postpone the commencing date — preferably at the beginning of a month — until they are. The first entry should be the closing reading on the last day of the month preceding that selected. This should be entered on the "spare" first line of the vehicle record so that from the first of the month onwards the resultant mileages are entered against the correct dates. Some drivers' log sheets make provision for opening and closing readings, but if the drivers find that this information is not being used they are apt to discontinue recording the same; consequently it is most important to brief them beforehand otherwise you may have to rely upon mileage estimates for the first few days which is never satsifactory. In practice, and provided you record daily mileages, the speedo' readings need only be entered on your record at the end of each working week. This saves time, enables you to ascertain that the speedo' is working, and provides. you with a means of correcting any errors made in subtracting opening readings from closing. Recording daily mileages is essential however, as they will enable you to calculate cost per job or trip, and for the haulier the rate to charge according to mileage even though his rates are calculated on a per ton basis or indeed on any other yardstick.

Fuel issued (agency/bulk) Provides for fuel drawn from "agency" sources and "bulk" storage. The fuel-tank capacity at the foot of the preceding column determines the cruising range of the vehicle according to the expected mpg, thus providing a check on the need or otherwise for purchasing fuel through agencies at a greatly increased cost; currently some 5p per gallon more than bulk storage. The vehicle tank capacity also determines the maximum gallonage that can legitimately be signed for at any one time.

Oil drawn (agency/bulk) As this is apt to be regarded as a relatively cheap item, drivers are often left to their own devices in maintaining the correct levels. However, oil is only as cheap as when it is used to avoid premature engine wear and/or costly seize-ups, so it is important to record all sump replenishments, including oil changes, in order to plug this potential profit leak. Furthermore, by recording drivers' names (column 7) you are able to identify any negligent culprits.

Operating costs/budgets Reproduced here are the final columns of the vehicle record, a section which now identifies the fleet /registered number, the make and P /D — meaning petrol or diesel — but most important of all the actual costs incurred as opposed to the budgets to be built in for each and every item of cost each month. Study these actual cost ingredients carefully, as you Will need access to each; establish the sources from which each can be obtained — particularly depreciation and establishment costs.

In next week's issue we will examine and compare the differences between actual and budgeted performances and costs, and consequently the need for budgetary control. Finally you can evaluate the uses to which costing or, more correctly, cost analysis, can be applied in formulating haulage rates, delivery charges, product or service prices and, by no means least, in plugging profit leaks.