SOLVING THE PROBLEMS DF 1 THE CARRIER r , URNING now from records of cost to the recording

Page 58

Page 59

If you've noticed an error in this article please click here to report it so we can fix it.

of gains, the first point to be noted is the difficulty of devising a system which will satisfactorily meet the needs of every haulier. At the one extreme, there is the jobbing haulier whose vehicles will rarely be more than 30 miles from headquarters and, at the other, the long-distance operator whose men and vehicles are, for the most part, engaged on journey work and who may be away from home sometimes several days at a time.

The best way to begin to consider the matter is from — the point of view of the order book. Every job must originate in an order and it is most important that all orders be properly entered.

For this purpose a day book is necessary. I have devised a ruling which will enable one book to serve both for the recording of orders received and of work done. Usually, two are presumed to be required. As, however, one of my objects is simplicity, I have eliminated the second book by embodying both sets of information in the one.

The suggested ruling is shown in Table 1. The columns are practically self-explanatory. If the work be such that it is generally difficult to give a precise statement of cost until after the job is finished, it may possibly be advisable to have two columns headed "charge," the first to be a tentative one and the second for the actual price. In some classes of work, too, it may be advisable to have a column for "rate."

By inserting a reference to the vehicle number, I provide all that is necessary to trace details of the work. It is necessary only to refer to the driver's record or the driver's waybill, which I shall shortly describe, relating to the vehicle named, on the date on which the work was executed, in order to ascertain of what the job actually consisted. The ledger reference is always p.dvisable, as it enables a check to be kept on the state of the customer's account. At predetermined periods the total revenue can be ascertained for the period in question by adding together the items in the column "charge."

The second step in any orderly method of carrying on the work of a haulage business is undoubtedly the issuing of proper instructions to the driver. It is, perhaps, unfortunate, in a way, that this involves additional clerical , work for that individual. The driver must make a daily return of the work he does with his vehicle, and in Table 2 is outlined a typical form for making such return in connection with local work.

The first point to which I should draw attention on this form is the provision, along the bottom, for records of speedometer readings, expenditure on petrol, oil and B44 sundries. This, on the face of it, looks like duplication, for, in the early part of this series and again in the issue of The Commercial Motor dated February 22, I have already made provision for that information to be noted on the official type of record.

I do not intend that this work should be duplicated, but have embodied provision for keeping these records on the form I am now discussing, to meet requirements of those who prefer not to enter that information on the official forms. If provision be made on the official records for those entries, the lower portion of the form shown in Table 2 can be omitted.

The next point to note is that as much as possible of the information required on this form should be entered in the office, so as to relieve the driver of mucli clerical work. The office, for example, can enter the name of the customer and particulars of the place and time of pick-up, also the number of the vehicle. In some cases, the entry of the work to be done can be made in the office, but, in that event, the driver should be warned that, if the work carried out be not entirely in accordance with the written instructions, he should correct accordingly before he presents his waybill to the customer for signature.

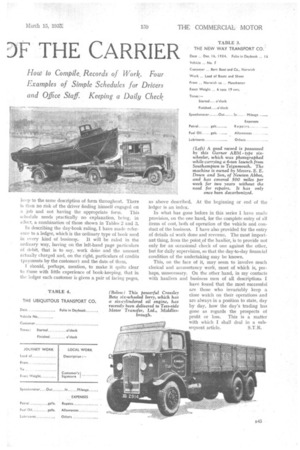

A waybill suitable for use in connection with operations concerned in the main, with journey work is indicated in Table 3. Here, again, most of the clerical work should be done in the office. The driver, however, must enter the exact weight and the times at which he starts and finishes. In this form, as in Table 2, provision is made for the entry of speedometer readings, consumptions of fuel and oil, and other expenses, and the same remarks apply, as in Table 2.

In Table 4 is shown a type of driver's waybill which is likely to suit the purposes of a firm whose vehicles may on one day be engaged on journey work and another on local deliveries. It is preferable, where possible, to keep to the same description of form throughout. There is then no risk of the driver finding himself engaged on a job and not having the appropriate form. This schedule needs practically no explanation, being, in effect, a combination of those shown in Tables 2 and 3.

In describing the day-book ruling, I have made reference to a ledger, which is the ordinary type of book used in every kind of business.It will be ruled in the ordinary way, having on the left-hand page particulars of debit, that is to say, work done and the amount actually charged and, on the right, particulars of credits (payments by the customer) and the date of them.

I should, perhaps, mention, to make it quite clear to those with little experience of book-keeping, that in ti-w ledger each customer is given a pair of facing pages,

as abovedescribed. At the beginning or end of the ledger is an index.

In what has gone before in this series I have made provision, on the one hand, for the complete entry of all items of cost, both of operation of the vehicle and conduct of the business. I have also provided for the entry of details of work done and revenue. The most important thing, from the point of the haulier, is to provide not only for an occasional check of one against the other, but for daily supervision, so that the day-to-day financial condition of the undertaking may be known.

This, on the face of it, may seem to involve much clerical and accountancy work, most of which is, perhaps, unnecessary. On the other hand, in my contacts with hauliers and business men of all descriptions I have found that the most successful are those who invariably keep a close watch on their operations and are always in a position to state, day by day, how the day's trading has gone as regards the prospects of profit or loss. This is a matter with which I shall deal in a sub sequent article. S.T.R.