ARRIVING AT A COSTINC SYSTEM FOR REPAIRS

Page 22

Page 23

If you've noticed an error in this article please click here to report it so we can fix it.

Solving the Problems of the Carrier A Method Adapted to a Particular Case Involving, Minimum ReqUirements and. Maximum Simplicity

A['TER some preliminary ifs and buts, which occupied all of the previous article, I now come to the practical details of this problem—to provide for the adequate recording of costs of maintenance and repair work carried out in a self-contained repair shop attached to a haulage business. The records are to be such that each vehicle is debited with the appropriate charge for work done upon it. The fleet comprises .11 vehicles, whilst the repair staff comprises a mechanic on full time and a carpenter whose services are available as and when required.

• It is a condition, specified in the inquiry, that the records shall be in such a form that a monthly return of the expenditure on each vehicle shall be made, the records to be in duplicate, one for the mechanic's own file, with the price column blank, •the other for the office with that column completed.

To this end, information is required under three heads— labour, materials and overheads. The details of the overhead costs are not, necessarily, for inclusion in this scheme of recording. The total is required so that it can be expressed as a percentage of the labour and material costs,

as will be -demonstrated. , An overriding condition, I think, is that the system must be as simple as possible, involving the minimum of clerical work.

• How to Record Maintenaoce Costs • A comprehensive scheme for recording maintenance costs will include the following:— .

(1) Job Card, on which there would be space for entry of a job number, date, number of vehicle, make and type, engine and chassis numbers, nature of repairs to be effected, materials required. From the information thus provided the repair-shop foreman will make his preparations for the work, All time and materials will be booked to the job number.

(2) Daily Time Sheets for the workmen. Each man will complete his own sheet daily, entering the times at which he commences each job and the time he ceases work on it. Thereference, in all cases, will be to the job number. On the time sheet there should be space for a description of the . work, and in that will he included a reference to the vehicle number.

(3) Stores Requisition. This is,a small docket to be used by the mechanic when he is obtaining supplies of material from the stores. Here again the job number will be the reference and there will be sufficient space on the docket to enable an accurate description of the materials to be entered, so that identification, so necessary for correct pricing, will be easy.

(4) The Cost Sheet, on which will be summarized the data contained on the daily time sheets and the stores requisition dockets. These will be entered separately in different parts of the sheet under " time " and " materials." There will be provision for the entry of the appropriate amounts to be • debited for overheads. The total of the entries on the cost sheet will be the expenditure on the particular repair covered by the job number and described originally on the job card. (5) A monthly summary for each vehicle of all the work described and costed on docket No. 4, relating to that vehicle, That series of five separate dockets is necessary for a complete system -of accounts in connection with a .moderatesize fleet and a repair depot of such proportion that several mechanics are employed, with a foreman in charge, and a storekeeper to look after the stores and issue the supplies. as and when required.

Something much simpler is all that is required" for the particular case which is under consideration. Here there is one mechanic only, who " doubles " the parts of mechanic, foreman and storekeeper. Obviously, it would be absurd to arrange for him, in his role of foreman, to prepare a job card and to issue that job card to himself as mechanic. Equally absurd is it for him to prepare a stores requisition as foreman, hand it to himself as mechanic, and take it back to himself as storelmeper when he wants materials. •

It is obvious, therefore, that a considerable amount of complication can be eliminated by short-circuiting these different parts of the system. Clearly, ills possible to cut out the job card, the daily time sheet and the stores requisition. That would leave us with dockets Nos. 4 and 5, the cost sheet and the monthly summary. The question arises: Is it possible to combine those two into one I think it is. The method would be to allocate one sheet per month ia each vehicle. The sheet must, obviously, be divided so as to allow separate entry for time and materials. It must be large enough to provide sufficient .space for the entry of all the work which, in the ordinary way, is likely to be carried out on one vehicle during one month, That would hardly be practicable on a sheet of reasonable size, if every little routine operation is to be so entered.

There should be room on an ordinary full-size sheet of notepaper for this, provided that the following expedient be adopted:—Allocate one sheet per month to cover the cost of routine operations—washing, polishing, greasing and oiling—in connection with all the vehicles, without distinction as to which is undergoing these operations. The total expenditure thus recorded is to be allocated throughout the fleet. • There is a double advantage in this arrangement. First, it achieves our immediate object. It makes it possible to enter all the sundry and non-routine repair jobs executed.

per vehicle per month on one sheet. Secondly, and certainly more important, it relieves the mechanic of the work of recording a series of small operations, the times needed to effect them, and the material used for each.

It is reasonable to expect that, all the year round, the time and the material used for such operations as washing and polishing, greasing and similar work will be the same per vehicle.. It is thus quite fair to average the total between them. The sheet set apart each month for the recording of this work can be given the title of " works," and the monthly total, divided by the number of vehicles,

can be added to the other expenditure on each :ndividuai vehicle.

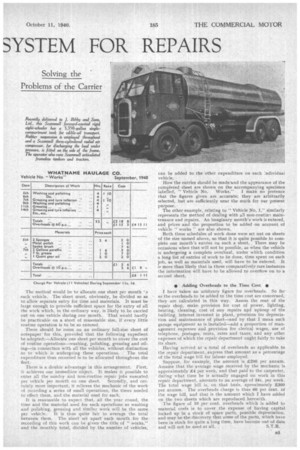

How the entries should be madeiand the appearance of the completed sheet are shown on the accompanying specimen

labelled, " Vehicle No. Works." I make no pretence that the figures given are accurate; they are arbitrarily selected, but are sufficiently near the mark for our present purpose.

The other example, relating to " Vehicle No. I," similarly represents the method of dealing with all non-routirvi maintenance and repairs. An imaginary month's work is entered, and prices and the proportion to be added on account of vehicle " works " are also shown.

Both these schedules of work done were set out on sheets of the size named above, so that it is quite possible to complete one month's entries on such a sheet. There may be occasions when that will not be possible, as when the vehicle is undergoing a complete overhaul, under which condition a long list of entries of work to be done, time spent on each job, as well as materials used, will have to be entered. It is more than likely that in those comparatively rare instances the information will have to be allowed to overflow on to a second sheet.

• Adding Overheads to the Time Cost I have taken an arbitrary figure for overheads. So far as the overheads to be added to the time cost are concerned, they are calculated in this way. Assess the rent of the repair shop, make provision for cost of power, lighting, heating, cleaning, cost of any repairs ad upkeep of the building, interest invested in plant, • provision for depreciation and maintenance of plant—and by that I mean such garage equipment as is installed—add a proportion of management expenses and provision for clerical wages, use of telephone, postages, rents, rates and taxes, and any other expenses of which the repair department ought fairly to take its share.

Having arrived at a total of overheads as applicable to the repair department,, express that amount as a percentage of the total wage •bill for labour employed. •

Suppose, for example, the amount is.. 21:10 per annum. Assume that the average wage received by the mechanic is approximately .E4 per week, and that paid to the carpenter, during what time he is actually engaged on work in this repair department, amounts to an average of 34s. per week. The total wage hill is, on that basis, aproxirna.tely 4300 per annum. The overheads charge is thus GO per cent, of the wage bill, and that is the amount which I have added on the two sheets which are reproduced herewith.

The figure of 10 per cent, overheads which is added to material costs is to cover the expense of having capital locked up in a stock of spare parts, possible depreciation, and may be the discovery that some of the parts, which have been in stock for quite a long time, have become out of date

and will not be used at all, S.T.R.