Solving the Problems The Simplest Way of of the Carrier

Page 29

Page 30

If you've noticed an error in this article please click here to report it so we can fix it.

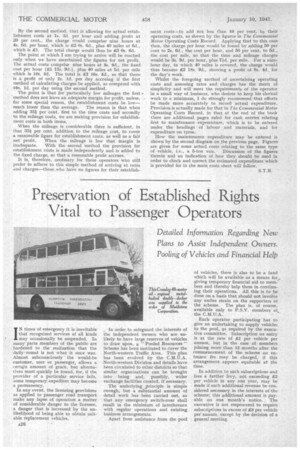

Keeping Costs Records T' AKE another look at the accompanying specimen page from The Commercial Motor Operating Costs Record; the figures which are shown theieen have Other uses than those,described in the previous article. The informatiort‘ can be used as a basis for assessing charges in a variety of ways.

Note that there are already available figures for cost per hour (time), and cost per mile (mileage). These figures, whilst they must not be used alone for assessing charges, as they contain no provision for either establishment costs or profit, are a foundation for the method of computing. ,rates by time and mileage. That is a method which is almost universally applicable.

One way to make provision for establishment costs and profit has already been demonstrated. It is the empirical or rule of thumb one of adding 33W per cent, to figures for operating costs, that percentage being sufficient, in average cases, to provide for establishment costs and leave 0 reasonable but not excessive margin of profit.

How the Operator Can Arrive at the Charge for Any Job Taking the figures shown, if 331 per cent. be added to 2s. ed.-the operating cost per hour-it gives us 3s. 4d., which is the charge per hour. Adding 331 per cent, to the M. per mile for running cost gives us ead. as the mileage

charge. The charge for any job of work which this operator is doing, that is to say, any job which involves from 80 to 100 miles per day, can be assessed by charging at the rate of '3s. 4d. per hour for every hour the vehicle is engaged and adding to that sum 6icl. per mile for every mile it is run.

Take, for example, the work done on Monday, December 2, when the vehicle ran for nine hours and during that period covered 100 miles. For nine hours the charge at 3s. 4d. per hour is £1 10s. ; 100 miles at WI. per mile is £2 16s. 3d.-the total is £4 6s. 3d. It is of interest to note that the charge per mile-arrived at by dividing £4 Cis. 3d. by 100, the Mileage run-is 10.45d., which, as near as makes no matter, is 10id.

Again, if the operator wishes to arrive at the price he should charge per ton, assuming he was actually carrying %

5 tons on this 5-ton vehicle, he divides the £4 6s. 3d. by five and finds that his charge ought to be 17s. 3d. per ton. It is to be observed that that may be a rate for a lead of 50 miles.

An alternative and more accurate method of calculating charges is to add, first, the actual establishment costs to the standing costs per hour and then to add a percentage for profit to the total of standing charges and establishment costs, that giving the basis for the time charge, and to add a percentage for profit to the mileage cost, thus achiev ing the rate per mile. , If it be assumed, in this case, that the establishment costs actually total £3 15s, per week that is nearly 1s. 3d. per hour. Adding that 1s. 3d. to the standing charge of 2s. 6d. per hour we get 3s. 9d. per hour as the total amount of fixed expenses per hour. Add 20 per cent, to that for profit-approximately 9d„-and a total_of 4s. 6d. is the charge per hour for time. Add also 20 per cent, to the 5d. per mile and we get ed, per mile for the charge for distance.

Now, assessing the job shown on Monday, December 2, on that basis I have nine hours at 4s. 6d. which is £2 Os. 6d., plus 1.00 miles at 6d. which is £2 10s. The total is £4 10s. 6d., as compared with £4 Os. 3d. as previously calculated.

Ascertaining the Net Profit from the Cost of the Job

It is of interest, before proceeding, to ascertain what is the actual net profit, assuming that the figure of is. 3d. per hour is correct for establishment charges. The actual cost to the operator of this particular job is nine times the 3s. 9d, for the fixed expenditure, which is £1 13s. 9d., plus 100 times 5d., the actual cost per mile (£2 Is. 8d.), a total of £3 15s. 5d.

If the operator charged according to the former method, arriving at his rate by adding 33* per cent, to the vehicle operating cost, then his net profit is 10s. 10d.

If he charged according to the second method, namely, by adding his establishment costs to the standing charge, and adding a fixed percentage to both those and the operating cost per mile, his profit is 15s. Id. The latter is not excessive for a day's work involving 100 miles of running with a vehicle of this description.

Here another important point arises. Suppose that on Monday, December 2, the vehicle to which these figures relate had covered 40 miles only instead of 100 miles with which it is credited in the data. What should the charge be for that day's work? By the first method, adding 33iper cent, to the operating cost, the charge would comprise that for nine hours at 3s. 4d. per hour, which is el 10s., plus 40 miles at 6'd. per hour, which is £1 2s. 6d., making a :total of £2 12s. 6d.

By the second method, that is allowing for actual establishment costs at 1s. 3d. per hour and adding profit at 20 per cent., the charge Would comprise nine hours at 4s. 6d. per hour, which is £2 Os. 6c1., plus 40 miles at 6d., which is -£1. The total charge would thus be £3 Os. 6d.

The point at which I am trying to arrive will be reached only when we have ascertained the figures for net profit. The actual costs comprise nine hours at 3s, 9d., the fixed cost per hour (£1 13% 9d.), plus 40 miles at 5d. per mile which is 16s, 8d. The total is £2 10s. 5d„ so that there is a profit of only 2s. ld. per day accruing if the first method of calculating charges be applied, as compared with 103. 1d. per day using the second method.

The point is that for particularly low mileages the first method does not leave an adequate margin for profit, unless, for some special reason, the establishment costs be low— much lower than the average. The reason is that when adding 331t per cent, first to the time costs and secondly to the mileage costs, we are making provision for establishment costs in both items.

When the mileage is considerable there is sufficient, in that 33-hper cent, addition to the mileage cost, to cover a reasonable figure for establishment costs, as well as a fair net profit. When the mileage is low that margin is inadequate. With the second method the provision for establishment costs is made independently and is added to the fixed charge, so that a reasonable profit accrues.

It is, therefore, necessary for those operators who still prefer to adhere to this simple method of arriving at rates and charges—those,who have no figures for their establish

rnent costs-to add not less than 50 per cent, to their operating costs, as shown by the figures in The Commercial Motor Operating Costs Record. Applying that to this case then, the charge per hour would be found by adding 50 per cent to 2s. 6d., the cost per hour, and 50 per cent. to 5(1., the cost per mile, so that the time and mileage charges would be 3s. 9d. per hour, plus 71.d. per mile. For a ninehour day, in which 40 miles is covered, the charge would thus become £2 18s, Od., showing a profit of 8s. 4d. for the day's work.

Whilst the foregoing method of ascertaining operating costs and assessing rates and charges has the merit of simplicity and will meet the requirements of the operator

• in a small way of business, who desires to keep his clerical work to a minimum, I do strongly recommend that efforts be made more accurately to record actual expenditure. Provision is actually made for that in The Commercial Motor Operating Costs Record, in that at the end of the book there are additional pages ruled for cash entrieS relating first to maintenance expenditure, which is to be entered under the headings of labour and materials, and for expenditure on tyres.

How the maintenance expenditure may be entered is shown by the second diagram on the previous page. Figures are given for some actual costs relating to the same type of vehicle, i.e., a 5-ton van. Discussion of the figures therein and an indication of how they should be used in order to check and cprrect the estimated expenditure which is provided for in the main costs sheet will follow.